➤ SIGNAL

A state attorney general filed a targeted complaint against a public multifamily REIT over fee structures that have been industry-standard for a decade. The fees aren't being challenged as excessive — they're being challenged as either illegal under existing rent caps or deceptive under consumer-protection law. That's a different category of risk than rent control.

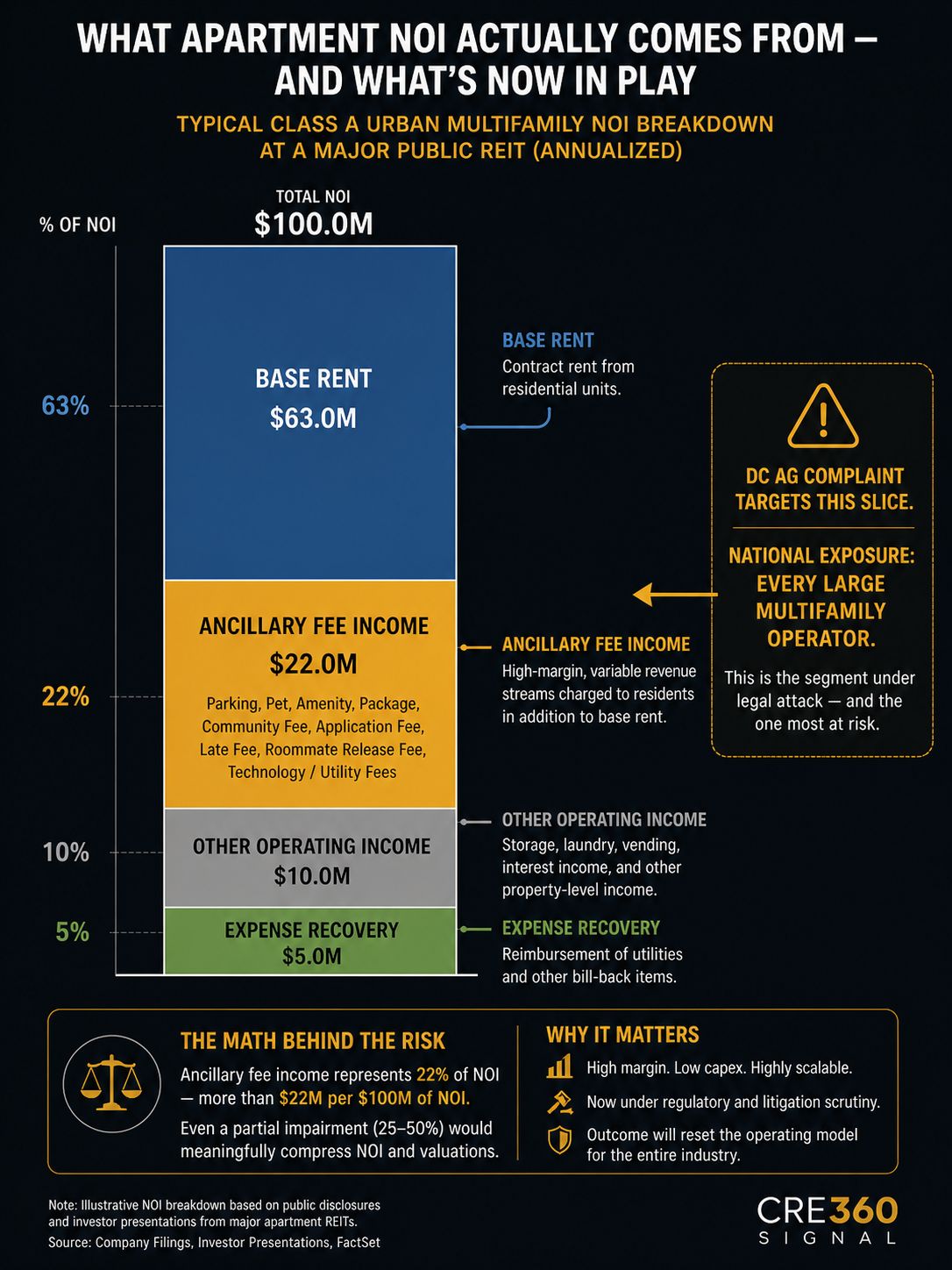

Most coverage of this story frames it as another junk-fee enforcement action — same family as the FTC's Greystar settlement and the RealPage cartel suits. The underwriting story is sharper: ancillary fee income is a meaningful component of NOI growth at every large public multifamily REIT, and the entire category is now in legal play. When AVB and EQR talk about "other income" on earnings calls, that's the line item DC is challenging. Underwriters who treat fee income as durable in 2026 acquisitions are pricing risk that's no longer there.

Implications for CRE:

Reset multifamily pro formas to assume fee income compresses 50–100 bps. That's not a Class A coastal problem — it's national. Suburban garden, urban Class A, Sun Belt mid-rise — all use the same fee playbook.

Acquisition models need a "fee impairment" sensitivity. Any buyer running a 2026 multifamily underwriting without testing what NOI looks like with a 30–40% haircut to ancillary income is asking the seller's broker to set their assumptions.

Greystar, Equity Residential, Camden, AvalonBay are obvious next targets. State AGs file in waves once a template complaint exists. DC just published the template — expect California, New York, Massachusetts, and Illinois to follow within four quarters.

The AVB/EQR merger logic gets reinforced. One of the unspoken drivers of consolidation is the legal/compliance cost of operating Class A apartments across jurisdictions with diverging fee rules. Scale absorbs that cost; mid-cap REITs and private operators eat it.

Operator-level systems need a rebuild. Property management software (Yardi, RealPage, Entrata) configured to maximize fee income by jurisdiction now needs to be reconfigured to defend it. That's a real capex line for any owner with a multi-state portfolio.

Subscribe to CRE 360 Signal™ Newsletter to Move Smarter in Today's CRE Market.

Subscribe to CRE 360 Signal™ Newsletter to Move Smarter in Today's CRE Market. Key Takeaways

- Trophy Manhattan office isn't recovering — it never broke. What's actually happening is the rest of the office stack is repricing downward while the top tier holds, and the spread between them is now wide enough to be the trade itself. Underwrite Class A and Class B as separate asset classes, not points on the same curve.

Never miss a Signal

Get the daily brief that busy CRE professionals rely on.