➤ SIGNAL

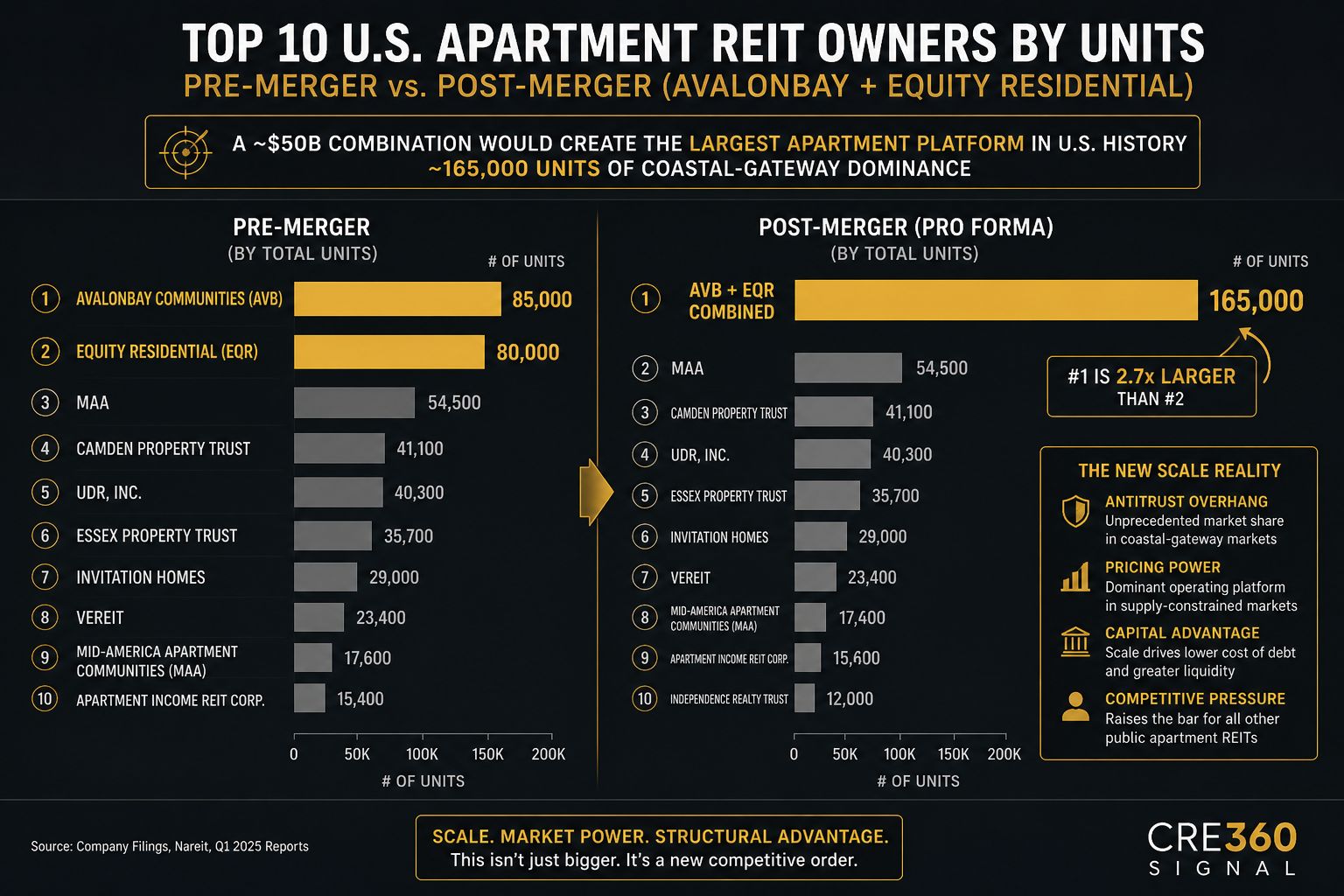

Two REITs that have spent fifteen years competing for the same renter on the same six blocks are now considering combining. That's not opportunism — it's a defensive posture. The trigger isn't valuation; it's the convergence of three forces hitting simultaneously: a persistent public-private NAV discount, a forced rebuild of revenue management infrastructure post-RealPage litigation (capex neither wants to absorb alone), and a 2026–2027 supply cliff that creates a narrow NOI-growth window worth fighting over from a position of scale.

The market read this as M&A; the more accurate read is consolidation as risk transfer. AVB and EQR aren't trying to grow — they're trying to absorb the cost of operating in a regulatory environment that's hostile to fee income (see DC AG vs. MAA), in a tech stack that needs to be rewritten, and in a debt environment where scale dictates spread. Merging is cheaper than fixing both balance sheets independently.

Implications for CRE:

New comp set. Any Class A coastal apartment trade in the next 18 months will be priced against the implied NAV of this transaction — even if it doesn't close.

Antitrust overhang. The first large public-REIT residential merger since the FTC tightened housing concentration scrutiny. Whatever happens here defines what's possible for Camden, MAA, UDR, and Essex.

Acquirer reset. Private equity buyers (Blackstone, Greystar, Cortland) lose two natural strategic competitors for premium coastal portfolios — bid depth shrinks, but cap rates harden.

Debt ceiling rewrite. The financing package on a $50B apartment platform sets the new benchmark for unsecured multifamily debt across the public REIT universe.

Operator margin compression normalized. The merger admits, structurally, that single-asset multifamily NOI growth no longer justifies the public-platform cost structure.

Subscribe to CRE 360 Signal™ Newsletter to Move Smarter in Today's CRE Market.

Subscribe to CRE 360 Signal™ Newsletter to Move Smarter in Today's CRE Market. Key Takeaways

- When the two largest pure-play apartment REITs would rather merge than compete, the message isn't bullish growth — it's that the cost of operating Class A multifamily as a public company has outrun the revenue model. Underwrite the next coastal apartment deal accordingly.

Never miss a Signal

Get the daily brief that busy CRE professionals rely on.