📢Good morning, today’s Signals are brought to you by CRE 360 Signal™.

Office-to-residential conversion has been discussed for decades. What makes the current moment different is not the concept itself, but the alignment of policy incentives, new financing tools, and a growing inventory of obsolete office buildings.

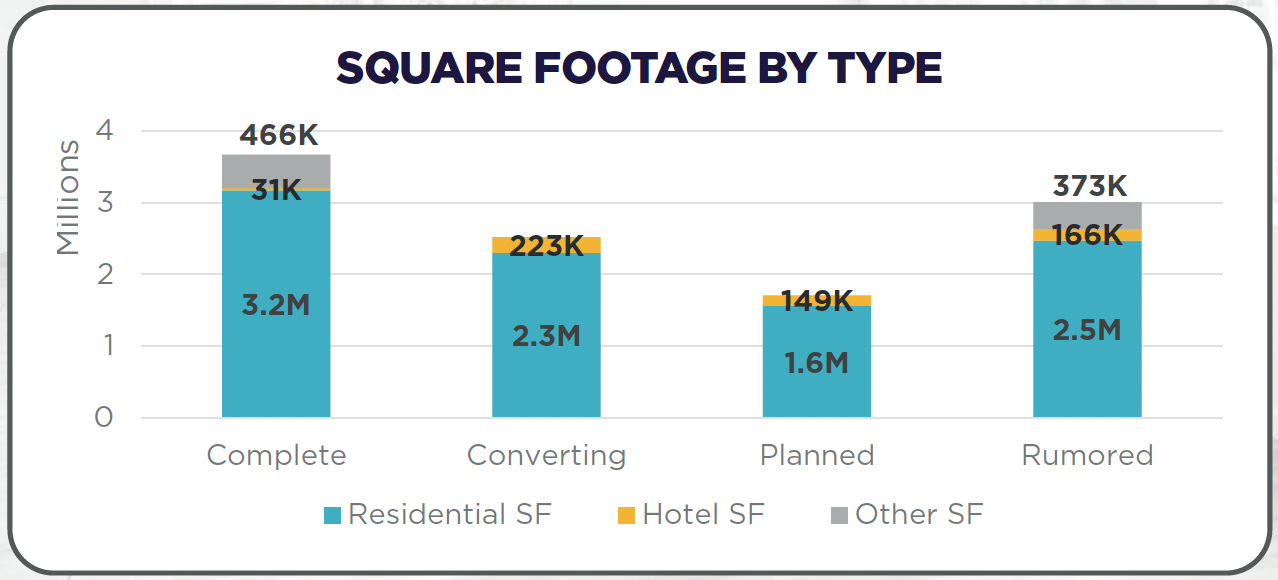

Washington D.C.’s latest conversion data illustrates the shift. More than 10 million square feet of office space is now completed, under construction, planned, or rumored for conversion, signaling that adaptive reuse is evolving from isolated projects into a repeatable redevelopment strategy.

➤ SIGNAL

Office Conversions Aren’t New — But the Capital Stack Is

Adaptive reuse has long been part of urban redevelopment, but it has historically remained limited.

The reason is simple: office buildings are not designed for housing. Deep floor plates, mechanical systems, plumbing infrastructure, and code requirements make many buildings difficult or uneconomical to convert.

As a result, only a small portion of office inventory is physically suitable for residential redevelopment.

What Makes This Moment Different

The Washington D.C. report highlights three forces that are now aligning in a way that did not previously exist.

Policy Incentives

Cities facing persistent office vacancies are beginning to actively engineer conversions. Washington D.C. introduced major incentive programs including:

“Housing in Downtown” — a 20-year property tax abatement

“Office to Anything” — a 15-year property tax freeze

These programs aim to attract investment and add 15,000 residents to downtown by 2028, positioning conversions as a core redevelopment strategy rather than a niche opportunity.

New Capital Structures

Financing has historically been the largest barrier to conversions. Developers are now increasingly using layered capital stacks that combine senior debt, incentives, and alternative financing tools such as C-PACE.

One major D.C. conversion recently secured $465 million in C-PACE financing, forming the backbone of a broader capital stack supporting a $750 million redevelopment. These structures are beginning to make large-scale conversions financially viable.

Permanent Office Obsolescence

The third factor is structural change within the office market itself. Many Class B and Class C office buildings built before 1980 are increasingly unable to compete with modern office space.

In Washington D.C. alone, analysts estimate roughly 20 million square feet of office inventory is functionally obsolete in today’s leasing market. Conversions therefore serve a new purpose: removing obsolete office inventory from the market.

Even if all planned conversions move forward, vacancy would decline only modestly—from about 22.8% to roughly 19%—illustrating that the office oversupply challenge remains significant.

Why This Matters Beyond Washington

If the combination of incentives, financing innovation, and redevelopment demand proves scalable, it could establish a repeatable playbook for other cities facing similar office challenges. Markets with aging office inventories — including New York, San Francisco, and Chicago — are already exploring similar strategies.

Conversions will not solve the office market’s structural issues, but they may gradually reshape downtown environments by:

reducing obsolete office supply

introducing residential density

stabilizing struggling office corridors

Key Takeaway

Office conversions are not a new trend. What is new is the growing recognition that a portion of the office inventory built in previous decades no longer fits the needs of modern cities.

Rather than waiting for demand to return, some markets are beginning to redesign their downtown cores around new uses. Washington D.C.’s conversion pipeline offers an early indication of how that transition may unfold.

CRE 360 Signal™ — Commercial Real Estate Intelligence

▼ EDITORIAL DESK TOP PICKS

Phoenix Multifamily Market Hits the Supply Crest. Record deliveries push vacancy higher as Phoenix apartments absorb demand but struggle to keep pace with new supply.

Construction Market Reality Check – Early 2026. Rising input costs, softer backlogs, and selective demand reshape the 2026 construction outlook.

Transaction Volume Is Back — But Don’t Confuse Activity with Recovery

Capital is re-entering the market, but pricing discipline—not momentum—is driving today’s transactions.Private Equity Continues Buying Public REITs — Take-private deals are accelerating as investors target undervalued listed real estate companies.

AI Is Reshaping Real Estate Decision-Making — Predictive analytics tools are rapidly transforming investment strategy and building operations.

Cybersecurity Risks Becoming Major Concern for Real Estate Firms — Increasing cybercrime is forcing property companies to upgrade digital protections.

CRE Investment Activity Expected to Rise 16% in 2026 — Market forecasts suggest a strong rebound driven largely by income returns rather than appreciation.

Industrial and Multifamily Expected to Lead CRE Recovery — Analysts see these sectors driving the next cycle while office recovery lags.

Apartment Market Showing Early Signs of Turnaround — Multifamily fundamentals may be stabilizing after rent declines in several markets.

Get Office Conversions Aren’t New — But the Capital Stack Is in your inbox

Why Washington D.C.’s latest office-to-residential pipeline signals a structural shift in urban redevelopment