➤ SIGNAL

A public hotel REIT just sold a 396-room full-service airport hotel for the cost of a basis-only renovation, then disclosed in the same release that it has $1.6B of mortgages coming due across the rest of the year. That sequencing isn't accidental — it's a forced seller telegraphing the next 12 months of dispositions to anyone willing to read the 8-K.

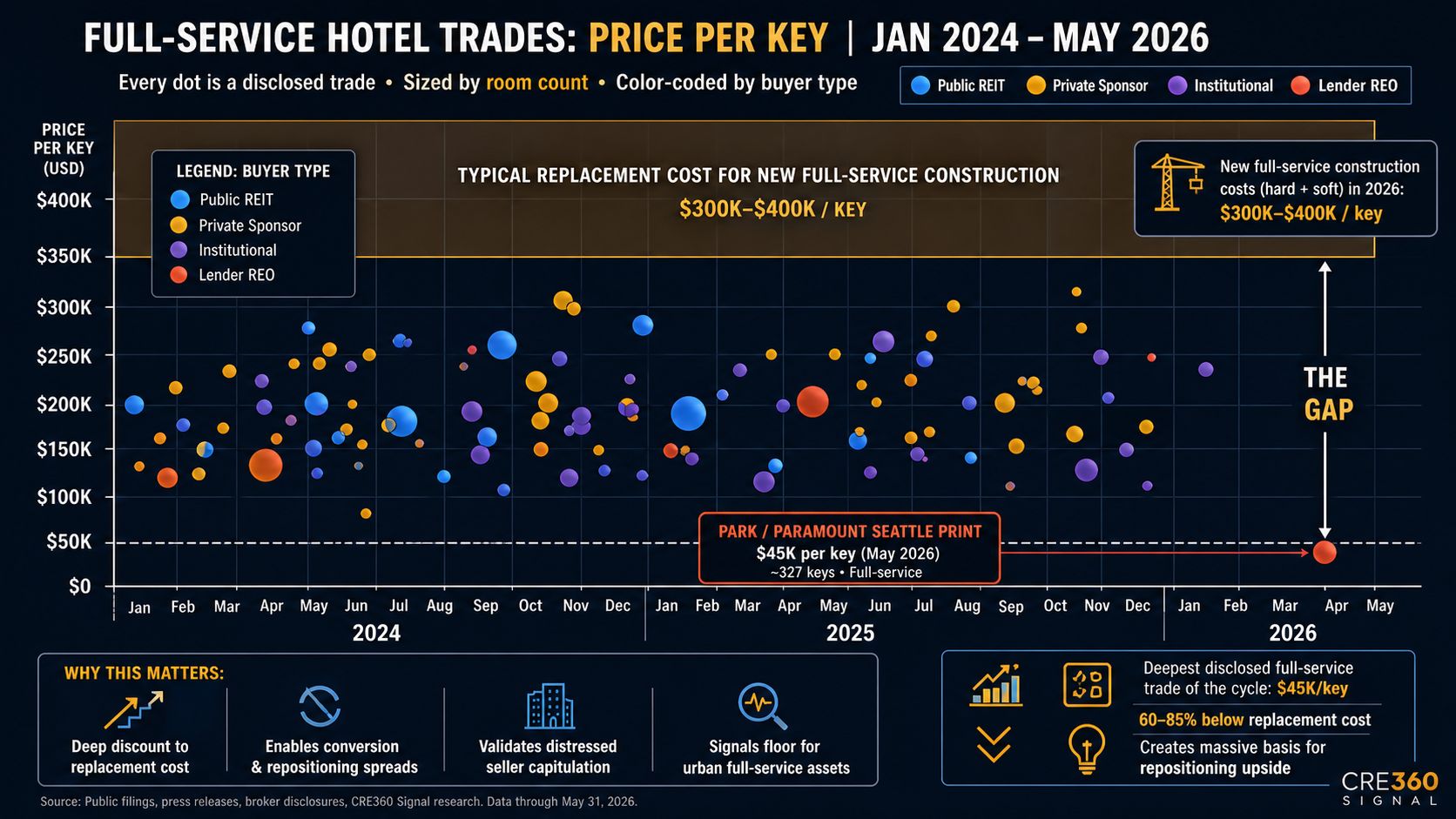

The headlines call this a strategic disposition. The underwriting story is sharper: Park is using the modestly improved 2026 transaction window to transfer capex-trap full-service collateral to local sponsors at sub-replacement basis before the maturity wall forces worse outcomes. The 16.3x EBITDA multiple looks fine on paper — but only because the math credits "avoided capex." Strip that out and the trade is closer to 8x on operating cash flow, with the buyer absorbing the PIP. That's the comp lenders and special servicers are now working with on every distressed full-service file in their pipeline.

Implications for CRE:

$45K/key is the new floor for older-vintage, heavy-PIP, secondary-CBD or airport full-service. Any seller pitching above that needs to defend the gap with renovated condition, brand, or in-place income — not "comparable trades."

The "EBITDA multiple inclusive of avoided capex" framing becomes the standard. Sellers who can't credit avoided capex into the multiple are admitting the asset doesn't trade at a defensible going-concern cap rate. Underwriters should reject the framing on stabilized assets and accept it only on capex-trap dispositions.

The public-seller / private-buyer dynamic is now the dominant hotel M&A trade. Local sponsors with renovation expertise and patient capital are the natural buyers; public REIT cost of capital can't justify holding the asset through a $30K/key PIP. Expect Pebblebrook, RLJ, Sunstone, and DiamondRock to follow with similar non-core prints.

The $1.6B maturity disclosure is a slow-burn capital event, not an acute one. Park has the access to refinance at the corporate level — but each individual asset-level loan that matures forces an asset-level decision: refi, recap, or sell. The 12 remaining Non-Core hotels are the answer to most of those decisions before they get asked.

Lender behavior is the watch item. A $45K/key public comp gives every special servicer holding distressed full-service paper a defensible mark for note sales, discounted payoffs, and deed-in-lieu valuations. Expect a pickup in note-sale activity in the second half of 2026.

Key Takeaways

- When a public REIT sells a full-service hotel for the cost of the renovation it was avoiding and discloses $1.6B in maturities the same day, the message isn't "strategic recycling" — it's "the rest of the queue is coming, and this is the price." Underwrite full-service acquisitions to that floor, not to the seller's broker pitch.

Never miss a Signal

Get the daily brief that busy CRE professionals rely on.