➤ SIGNAL

This is the cleanest supply-demand setup in CRE right now.

Demand is demographic and non-discretionary; supply is frozen by the same costs and rates throttling everything else.

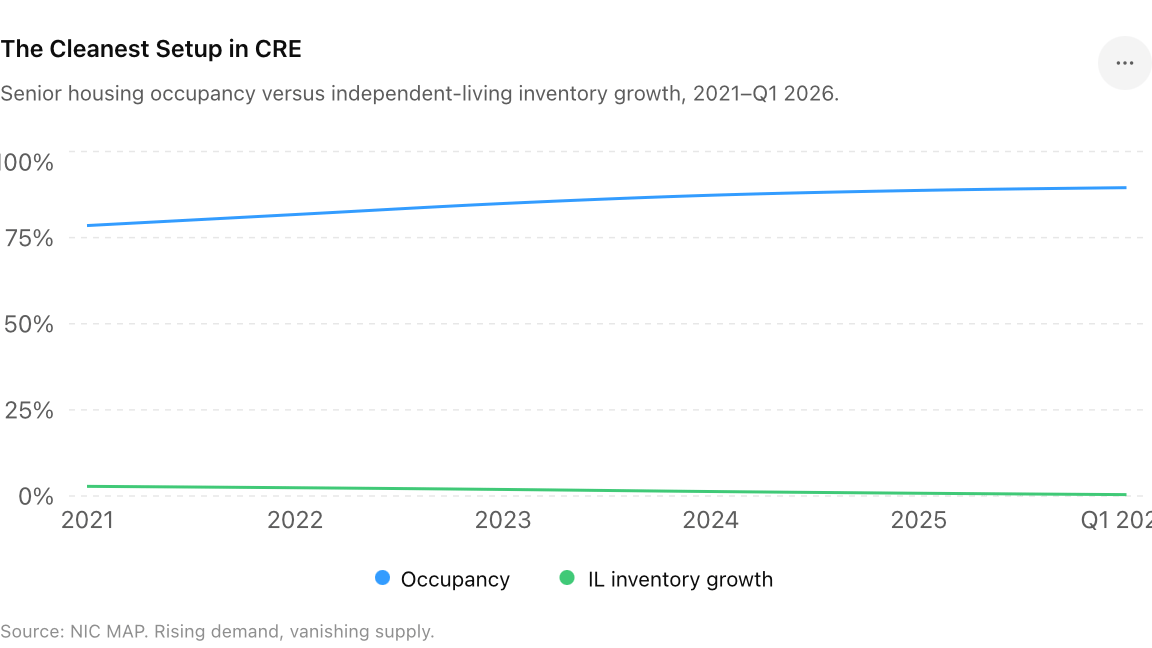

The 80+ cohort is inflecting now, and that demand doesn't wait for a rate cut. Meanwhile the construction math that killed ground-up everywhere also killed new senior-housing starts — inventory growth at 0.4% is effectively a development stop. Occupancy climbing 19 straight quarters into that void is a textbook rent-power setup.

Capital has read it correctly: a decade-high volume print and the largest opportunistic fund in Kayne Anderson's history, both pointed at the space.

Implications Operators with stabilized assets hold pricing power into 2027. The residual risk is operational — labor and care intensity — not demand. Underwrite the operator, not just the real estate.

Key Takeaways

- Demographics set the demand; a frozen pipeline hands operators the pen on rent.

Source: The Real Deal / CRE Daily / NAIOP — 2026 · Office · Multifamily · Adaptive Reuse

Never miss a Signal

Get the daily brief that busy CRE professionals rely on.