Net-Lease Cap Rates Tick Up as the Fed Takes Its Rate Cut Off the Table

Retail single-tenant yields rose to 6.60% in Q2 after the Fed dropped a 2026 cut from its projections.

CRE 360 Signal Editorial Desk·Jul 16, 2026

Debt, equity & transactions

Retail single-tenant yields rose to 6.60% in Q2 after the Fed dropped a 2026 cut from its projections.

New deliveries head for a decade low just as big capital moves in.

Green Street's June index gains 4.1% for the year — and stays 14% under peak because cap rates won't move.

A persistent public-market discount keeps pulling listed real estate into private and consolidated ownership.

JLL's new credit index hits an all-time high as lenders fight to place capital.

Altus says performance has split to a record spread as $875B in loans come due — and retail, not office, is leading.

The new Fed chair's first pause confirms there's no rescue cut coming for $875B of maturing CRE debt.

Median CRE just hit an all-time high — but the aggregate is hiding a record split between winners and losers.

10 Hudson Yards lines up a $1.4B refi — and sets the mark for trophy office debt.

Legal frameworks now define how real assets move on-chain, enabling institutional capital to scale tokenized ownership structures across multiple asset classes.

Escalating Iran conflict begins transmitting through fuel, supply chains, and investor behavior into U.S. real estate decisions.

Global brokerage consolidates capital-markets power with major U.S. advisory acquisition.

CBRE Investment Management just hit a major institutional milestone in how capital moves through real estate markets — and it signals where big‐ticket liquidity may be flowing next.

Cloud and AI tools target forecasting accuracy and grid reliability

Dissenting Fed voice argues policy remains overly restrictive as inflation cools.

Tightening spreads point to improving risk appetite before deal volume responds

realty-income-citycenter-preferred-equity

JPMorgan has moved its expected first Fed rate cut to December 2025, shifting it forward by a month and triggering an immediate repricing across futures markets.

2026 U.S. CRE loan maturities spark uneven distress across asset classes, with office and retail risks testing lender resilience.

Retail retreat from equity dips shifts market resilience to institutional ETF flows, signaling new volatility risks for capital markets.

Modest yield decline signals two-speed bond market as investors hedge on delayed economic data, influencing CRE capital costs.

Trophy assets lure global capital while weaker offices face a slow, disciplined recovery.

Stabilized fundamentals and capital discipline are redefining the retail property cycle.

Second rate cut in two months trims borrowing costs and reignites liquidity across U.S. CRE.

A 54% YoY sales jump and $1.1 B trophy trades mark a pivotal re-pricing phase in NYC’s CRE recovery.

Population-fueled demand and selective capital discipline keep Florida’s CRE cycle in expansion mode.

Lower yields reduce friction in CRE financing; buyers re-engage while lenders keep covenants tight.

Lower occupancy costs and resilient in-migration keep pricing power tilted to owners—insurance remains the wild card.

Distress signals jump from abstract to benchmark as 1100 Superior resets Midwest office comps.

$140 B in foreign bets on Chinese real estate are unraveling, forcing fire sales and prompting a global capital retreat toward safer markets.

Demand normalizes; capital insists on discipline.

Foreign inflows are recalibrating toward yield, governance, and gateway safety as capital costs reshape cross-border strategy.

Powell’s signal that quantitative tightening may end reshapes debt costs and sentiment across real estate finance

Banker departures and M&A contraction signal leaner underwriting conditions across capital markets and CRE.

Degag collapse deepens Europe’s real estate credit strain, prompting tighter underwriting and exposure limits.

Green Street’s CPPI edges up, confirming pricing equilibrium and renewed deal flow in U.S. commercial real estate.

A $180M Manhattan loan default pushed office CMBS delinquencies above 8%, reshaping lender risk across the Northeast.

Yields stabilize near 6.8% as investors reengage across net lease sectors.

Lower policy rates ease borrowing costs, but CRE loan distress and tight credit temper optimism.

$27.7 B in CRE loans reworked amid 7% refinancing rates and maturing 2025 debt.

New disclosure rule lets modified CRE loans disappear from public view after 12 months, masking true debt stress.

Lenders are extending maturities to avoid defaults, doubling CRE loan modifications and deferring risk into 2026–2028.

Large-scale recap confirms lender confidence in necessity retail’s income stability.

Prices stabilize; modest volume rebound supports underwriting discipline.

Federal paralysis halts permits, data, and loan programs—raising execution risk and widening spreads across U.S. commercial real estate.

Divergent sectors force Fed to prioritize inflation control over property market relief.

CRE transaction volumes up 10% in 2025 as rates plateau, drawing capital back to multifamily, industrial, and debt-backed dealmaking.

Class A assets attract bids near peak while transitional deals sit idle.

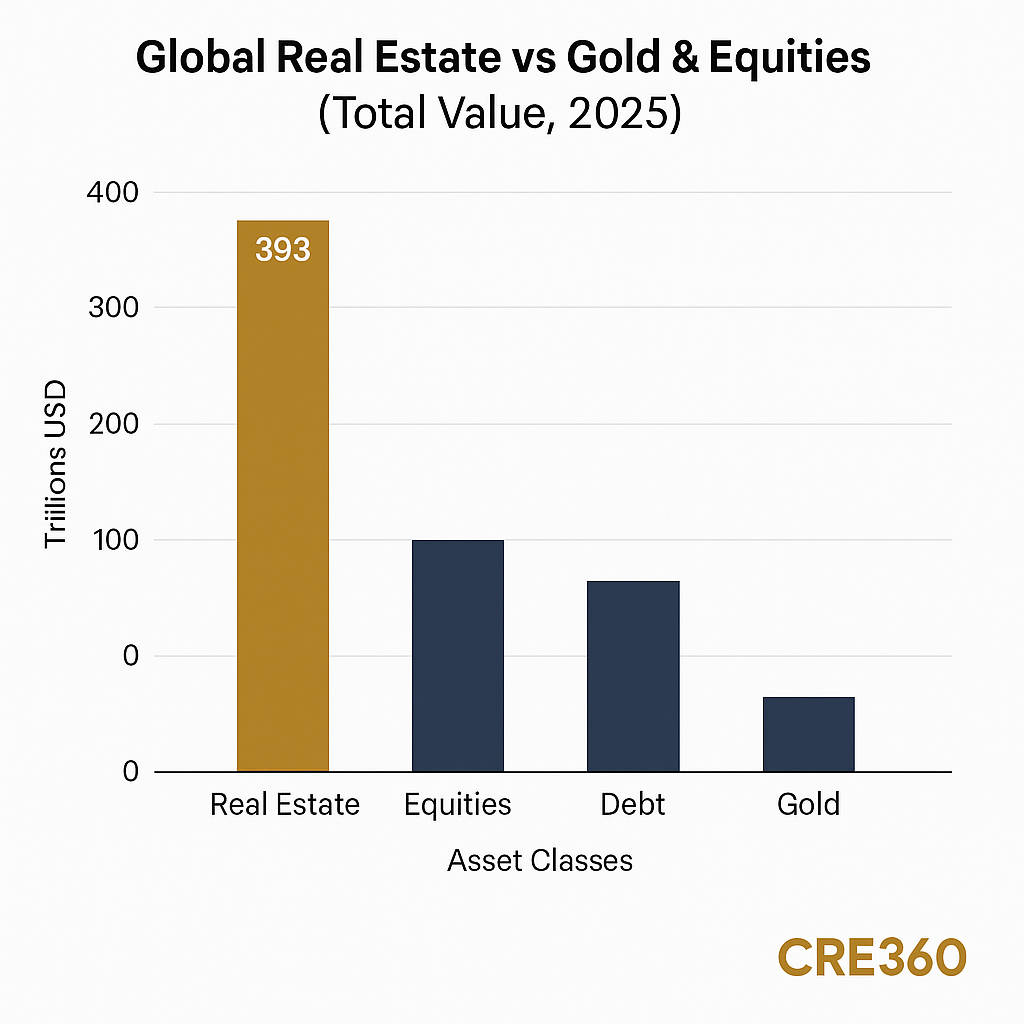

Property is the world’s largest store of wealth — quadruple global GDP and 20× the value of all gold.

State restrictions and waning foreign allocations leave U.S. property reliant on domestic syndicates.

Record deals, double-digit yields, and Golden Visa inflows keep Dubai ahead of global peers.

Shrinking foreign inflows leave U.S. CRE reliant on selective capital and domestic syndicates.

Investors pivot from secondary retail toward AI, ESG-compliant assets as capital reallocates globally.

Illiquidity deepens as capital shuns equity, favoring debt; stranded assets face stalled sales.

Early 2025 leasing and survey data signal a tentative floor for B/C office pricing and demand.

First rate cut in years reduces financing drag, setting stage for renewed deal flow and selective cap-rate relief.

Marathon’s Richards sees rate cuts driving buyouts, private credit, and CMBS demand.

First major public-to-private office deal signals patient capital returning to NYC and SF trophy towers.

Swift leadership transition signals governance strength and renewed liquidity for CRE’s largest private

Big-check capital targets manufactured housing for durable yields and low capex.

Origination and issuance tick up as non-banks re-enter; banks stay selective, terms improve modestly for well-structured deals.

PJM capacity costs jump 6× as hyperscale projects flood Pennsylvania, raising financing risk for CRE linked to power-intensive users.

Public-private deal unlocks stadium plus 6,000 homes; muni bonds fund infrastructure, private equity funds venue.

MSCI data shows first back-to-back annual gains since 2022

Fed's anticipated rate cut to lower borrowing costs, impacting CRE financing positively.

Three rate cuts in 2025 expected; impacts CRE cost of capital and financing plans.Date & Sources: September 12, 2025. Reuters, Morgan Stanley, Deutsche Bank.

Brent drops to ~$67, WTI ~$63 as inventories build; logistics see marginal cost relief but weak demand looms

Softer PPI and labor revisions pushed spot gold to ~$3,637/oz, just shy of a fresh high. Markets lean to a September cut as the 10-year grazes 4%.

Consumer prices overshot expectations, but labor weakness keeps the Fed on track for a likely September rate cut.

30-year mortgage rates dropped to 6.49%, the lowest since October 2024. Refinancing surged and purchase applications gained, signaling a rate-sensitive rebound in demand.

Regional banks remain cautious on CRE, pushing more flow to private credit.

Cottonwood raises $1B “special situations” fund, doubling target as investors chase distress opportunities in a frozen CRE market.

Yen weakens after PM resignation, Nikkei rallies, gold near records. Stronger USD/JPY reshapes inbound tourism and Japanese capital flows into U.S. CRE.

Markets now assign ~90% odds to a September Fed cut, with some banks calling 50 bps. Relief boosts refi math but doesn’t change long-run cap-rate expectations.

Spot gold holds just below all-time highs, reflecting rate cut expectations and macro caution. Allocators are tilting into real assets and secured credit, creating knock-on signals for CRE capital flows.

The RCA CPPI turned positive again. Two straight YoY gains signal a floor, led by retail and industrial while office bifurcation persists

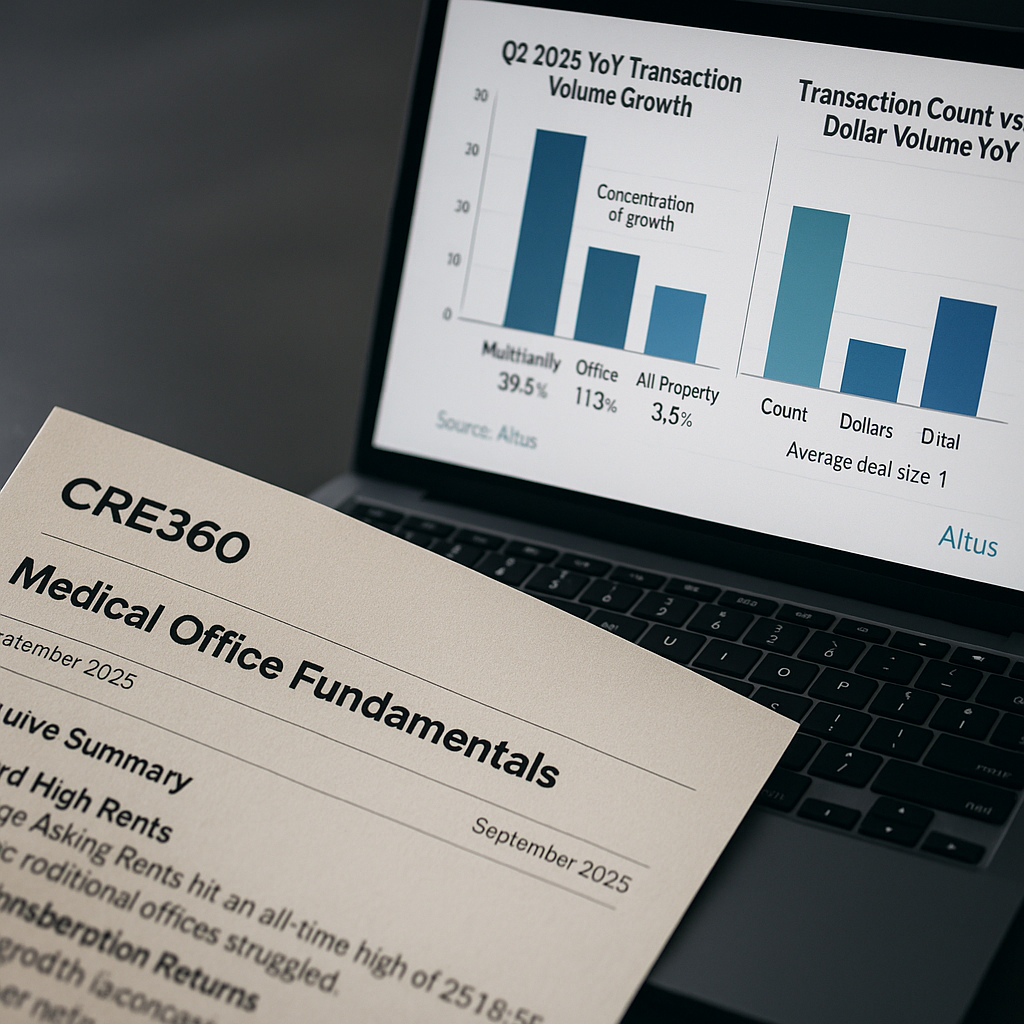

Dollar volume rose even as the market did fewer trades. Large, institutional deals carried Q2 while small and mid-market liquidity thinned. Sep 2025. Source: Altus Group Investment Trends Report (Q2 2025).

Incremental gains show market resilience; debt costly but available keeps transactions flowing.

JLL reports lifestyle office markets command 32% rent premiums, twice-as-fast lease-ups, and lower vacancy—signaling a structural shift in office demand.

Nomura revives CMBS platform with Barclays veterans, targeting trophy assets as U.S. banks retrench.

Austin-based firm overshoots targets, signaling LP confidence in mid-market operators despite higher

The nation’s largest apartment manager is rolling out pricing calculators, AI tools, and resident-facing transparency measures to sustain NOI in a cooling rental market.

Norwegian Wealth Fund acquires Midtown Tower at 34% discount, signaling major NYC office market shift and key investment trend in commercial real estate.

U.S. commercial real estate investment sales surge 16% in H1 2025, with $163.6B in transactions as private buyers drive market recovery amid selective price stabilization.

Commercial real estate lending rebounds in Q2 2024, with 66% year-over-year growth as banks and debt funds return to market, driven by stabilizing rates and improved underwriting confidence.

Sources: Altus Group, GlobeNewswire, GlobeSt

Trusted Daily

40,000+

Daily Subscribers

Brokers, investors, developers, and lenders open CRE 360 Signal™ every morning for the market intelligence that moves their decisions.

Free. Independent. Editorially rigorous.

Follow the Signal

Add your profile URLs from the Editorial Desk → Social links.