📢Good morning, today’s Signals are brought to you by CRE 360 Signal™.

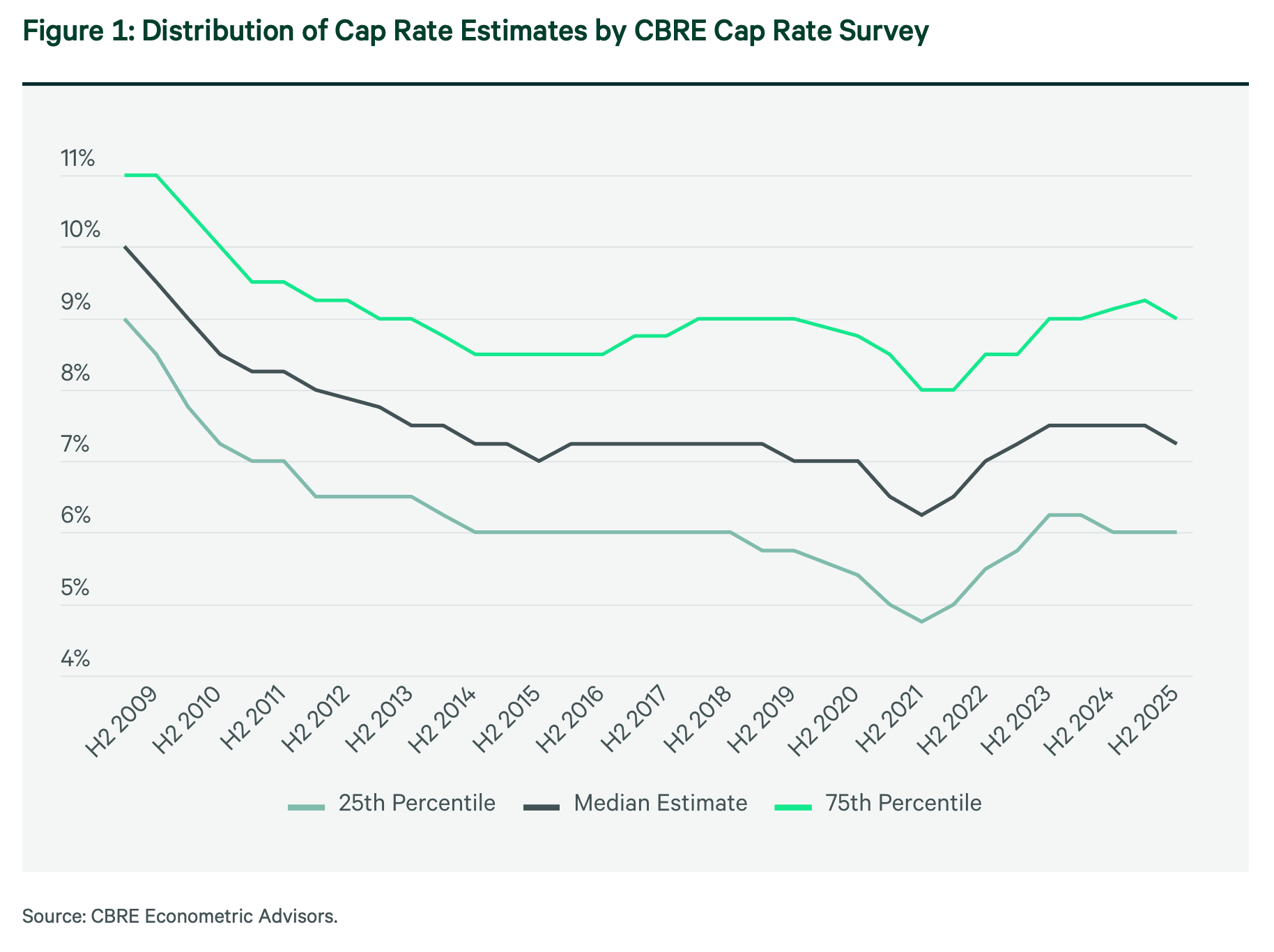

A recent cap rate survey from CBRE indicates that U.S. commercial real estate pricing may be entering a new market phase. The survey shows historically wide dispersion between cap rate estimates across property types and markets, largely driven by elevated cap rates for Class B and C office assets. At the same time, survey responses suggest early signs that cap rates at the upper end of the range may be stabilizing or beginning to decline. Respondents also reported growing expectations that cap rates could decrease over the next six months, potentially supporting increased transaction activity.

🎧 Busy to read? Catch the Daily Podcast (Subscribe on YouTube, Apple, Spotify)➤ SIGNAL

Recent Cap Rate Survey published by CBRE Econometric Advisors suggests that the U.S. commercial real estate market may be transitioning into a new cycle following several years of pricing uncertainty and reduced transaction activity.

CBRE has conducted its biannual cap rate survey for 17 years, gathering estimates from capital markets professionals across multiple U.S. markets and property sectors. The survey aims to capture market-clearing cap rate expectations based on real-time insights from brokers and investment professionals actively involved in transactions.

According to the survey, the distribution of cap rate estimates across markets remains unusually wide. The spread between the 25th percentile and the 75th percentile of estimates is near record levels. This dispersion reflects significant differences in risk perception and growth expectations across asset classes.

A major contributor to this spread is the continued weakness in Class B and Class C office properties. These assets are generally being priced at significantly higher cap rates due to structural demand challenges and increased vacancy levels in many office markets.

Despite the wide dispersion, the survey also indicates early signs of stabilization at the higher end of the cap rate range. Cap rate estimates at the 75th percentile have begun to show modest declines, suggesting that pricing for higher-risk assets may be approaching a peak.

Survey respondents also reported growing expectations that cap rates may decline during the next six months. If realized, this shift could signal improving investor sentiment and potentially support increased investment activity across commercial real estate markets.

The findings suggest that the market may be moving toward greater price discovery after a period characterized by limited transactions and significant valuation uncertainty.

Key Takeaway

The CBRE cap rate survey indicates that while pricing differences across asset classes remain significant, market participants are beginning to see early signs of stabilization in commercial real estate valuations. If expectations of declining cap rates materialize, the sector could see increased transaction activity and improved investment returns as the market moves further into its next cycle.

CRE 360 Signal™ — Commercial Real Estate Intelligence

▼ EDITORIAL DESK TOP PICKS

Amazon Plans Major Office Footprint Reduction — The tech giant is preparing to shrink its office portfolio significantly as AI and hybrid work reshape space demand.

Banks Boost Apartment Lending Even as Troubled Loans Increase — Lenders are expanding multifamily lending despite rising CRE distress in other sectors.

CRE Transaction Activity Projected to Top $66B Early in 2026 — Market data suggests a modest recovery in early-year deal volume across major property sectors.

Private Equity Continues Buying Public REITs — Take-private deals are accelerating as investors target undervalued listed real estate companies.

AI Is Reshaping Real Estate Decision-Making — Predictive analytics tools are rapidly transforming investment strategy and building operations.

Cybersecurity Risks Becoming Major Concern for Real Estate Firms — Increasing cybercrime is forcing property companies to upgrade digital protections.

CRE Investment Activity Expected to Rise 16% in 2026 — Market forecasts suggest a strong rebound driven largely by income returns rather than appreciation.

Industrial and Multifamily Expected to Lead CRE Recovery — Analysts see these sectors driving the next cycle while office recovery lags.

Apartment Market Showing Early Signs of Turnaround — Multifamily fundamentals may be stabilizing after rent declines in several markets.

Get Survey Signals Possible Turning Point in Commercial Real Estate Pricing in your inbox

Wide cap rate dispersion persists, but CBRE survey suggests stabilization emerging as investors anticipate declining cap rates and renewed transaction activity.