📢 CRE 360 Signal™.

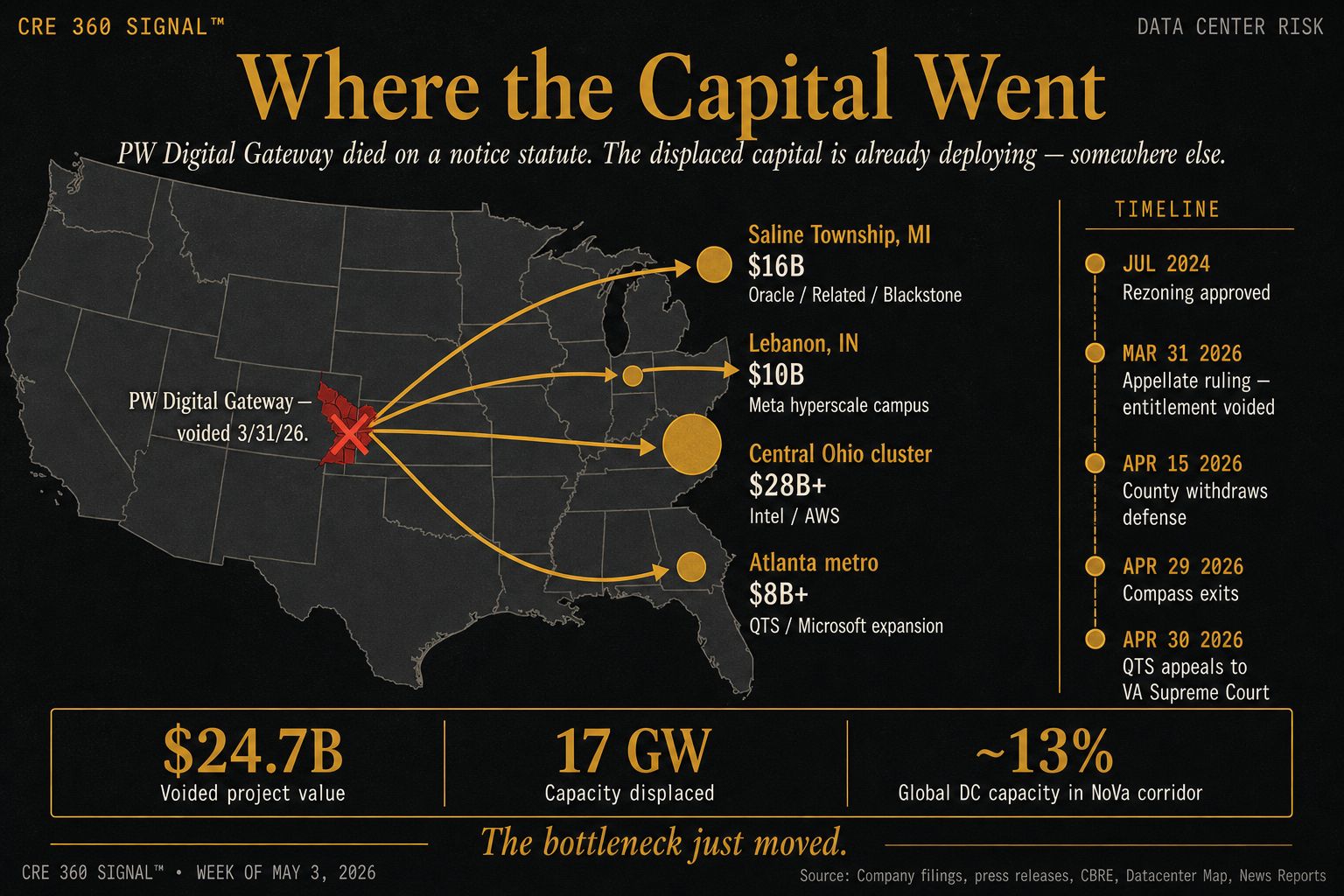

Compass Datacenters walked away from the 2,100-acre PW Digital Gateway near Manassas Battlefield on April 29 after losing on procedural notice grounds at the Virginia Court of Appeals. Power was supposed to be the binding constraint on AI infrastructure. Entitlements just became the second one — and that changes where the next $50 billion of hyperscale capital deploys.

🎧 Busy to read? Catch the Daily Podcast (Subscribe on YouTube, Apple, Spotify)➤ SIGNALS

On April 29, Compass Datacenters formally exited the 2,100-acre Prince William Digital Gateway project, declining to appeal further after the Virginia Court of Appeals voided the rezoning on March 31. The court's ruling didn't strike down the project on environmental, NIMBY, or political grounds — it killed it on a statutory technicality, finding that the public notice issued under VA Code §15.2-2204 was procedurally defective.

Two weeks earlier, Prince William County's Board of Supervisors withdrew its own defense after burning $1.72 million in taxpayer funds on the litigation. The local government partner abandoned the developer mid-fight. Hours before the April 30 appeal deadline, Blackstone-owned QTS filed a notice of appeal to the Virginia Supreme Court — a last-minute attempt to keep a sliver of the project alive.

The voided entitlement covered roughly 17 GW of planned capacity in a corridor that already hosts about 13% of global data center capacity. The same week the project died, Equinix disclosed in its Q1 earnings that power — not space — has become the binding constraint on hyperscale growth. PW Digital Gateway proves the binding constraint is now bifurcated.

Every data center underwriting model in 2026 was built around two risks: power availability and tenant credit. This ruling adds a third — latent statutory-notice risk that survives the entitlement closing by years. That's a category of risk most developers, lenders, and title insurers don't currently price. The PW Digital Gateway didn't fail because the project was bad. It failed because Virginia's notice statute is more demanding than the county process assumed, and an appellate panel was willing to enforce it strictly. For the first time in a major U.S. data center market, an appellate court voided a multi-billion-dollar entitlement on procedural grounds — and capital responded by leaving.

Implications for CRE

Title insurance and entitlement reps tighten across the asset class. Expect lender-side counsel to demand independent statutory-notice opinions on every Northern Virginia rezoning closed in the last 36 months — and to extend that diligence to other major data center jurisdictions.

Capital migrates to cleaner entitlement records. Saline Township, Lebanon, Central Ohio, and Atlanta metro accelerate. The Midwest hyperscale corridor — already absorbing $26 billion in announced capex this year between Oracle/Related Michigan and Meta Indiana — becomes the de facto Tier-1 alternative to Northern Virginia.

The bottleneck migrates from physical to legal. Equinix says power is the binding constraint. PW Digital Gateway proves there are now two binding constraints, and the legal one cannot be solved by writing a bigger check.

Land basis in the Loudoun-Manassas corridor reprices downward. Sellers holding entitled positions in NoVa just watched the most aggressive comp evaporate. Buyers either repricing or moving to tertiary markets — neither is good for incumbent landowners.

Key Takeaways

Entitlement risk doesn't end at the rezoning vote anymore — it ends when the appellate clock runs out, and that can be years later. For data center developers, lenders, and the secondary market for entitled land, the PW Digital Gateway ruling changes which jurisdictions are actually worth paying premium basis to enter.

CRE 360 Signal™ — Commercial Real Estate Intelligence

▼ EDITORIAL DESK TOP PICKS

🏢 Office / Leasing / Urban Markets

WTC district now rivals Midtown with $140+ rents — Downtown Manhattan leasing has surged, pushing rents above $100–$160 PSF with ~95% occupancy.

Office towers selling at up to 95% discounts — Distressed office assets across major cities are trading at fractions of prior values, signaling structural repricing.

Dallas office building sale tied to renovation strategy — A 115K SF office asset is being repositioned to Class A quality amid ongoing demand shifts.

⚡ Industrial / Data Centers

$2B data center expansion in Texas backed by Oracle demand — DataBank is scaling a 600K SF campus with 180 MW capacity, reflecting AI-driven infrastructure demand.

ICE warehouse acquisitions creating new CRE asset class — Federal purchases of industrial assets for detention facilities are reshaping warehouse demand and pricing.

🔗 https://www.wsj.com/business/logistics/ice-dhs-detention-center-warehouses-ac0af8e4

🏗️ Development / Mixed-Use / Adaptive Reuse

Dodgers stadium land seen as major CRE development opportunity — Large-scale mixed-use potential tied to transit infrastructure could unlock billions in value.

Oceanwide Plaza $470M deal faces financing and legal hurdles — One of LA’s largest stalled projects continues through bankruptcy with multiple bidders.💰 Capital Markets / Debt / Regulation

Fed examining banks’ exposure to private credit funds — Regulators are concerned about growing links between banks and nonbank CRE lending structures.

Private credit exposure flagged as “growing and opaque” — CRE lending risk is increasingly shifting outside traditional banking channels.

🏢 Brokerage / Industry Structure

Re/Max to be acquired in ~$880M deal — Consolidation continues as tech-enabled brokerages scale nationally.

🌍 Market Trends / Investment Signals

CRE increasingly tied to AI and tech infrastructure demand — Data centers are becoming one of the fastest-growing asset classes globally.

95% of investors planning increased data center allocation — Institutional capital is aggressively shifting toward digital infrastructure.

Office leasing showing early recovery signals in multiple markets — Positive absorption is spreading across U.S. metros despite elevated vacancy.

Luxury retail expansion up 65% year-over-year — High-end retail is outperforming due to resilient high-income consumers.

🏠 Housing / Multifamily / Spillover Effects

Housing slowdown creating buying opportunity for investors — Reduced competition and slower sales are improving acquisition conditions.

Mortgage rates stabilizing around 6.3%–6.5% range — Elevated but predictable rates are shaping acquisition and development strategies.

🏦 Macro / Structural CRE Shifts

CRE debt market now exceeds $5 trillion — Banks still dominate but non-bank lenders continue gaining share.

Banks hold ~$1.89T of income-producing CRE loans — Traditional lenders remain core but are losing relative dominance.

🏬 Retail / Experiential / Distress

American Dream mall faces $800M debt dispute — Bondholders allege manipulation of property value amid financial stress.

Saks Fifth Avenue closing stores tied to CRE restructuring — Retail bankruptcies continue to reshape mall tenancy and valuation dynamics.

Get The Bottleneck Just Moved in your inbox

A Virginia appellate ruling killed a $24.7B data center project on a notice technicality — and rewrote the underwriting checklist.