➤ SIGNAL

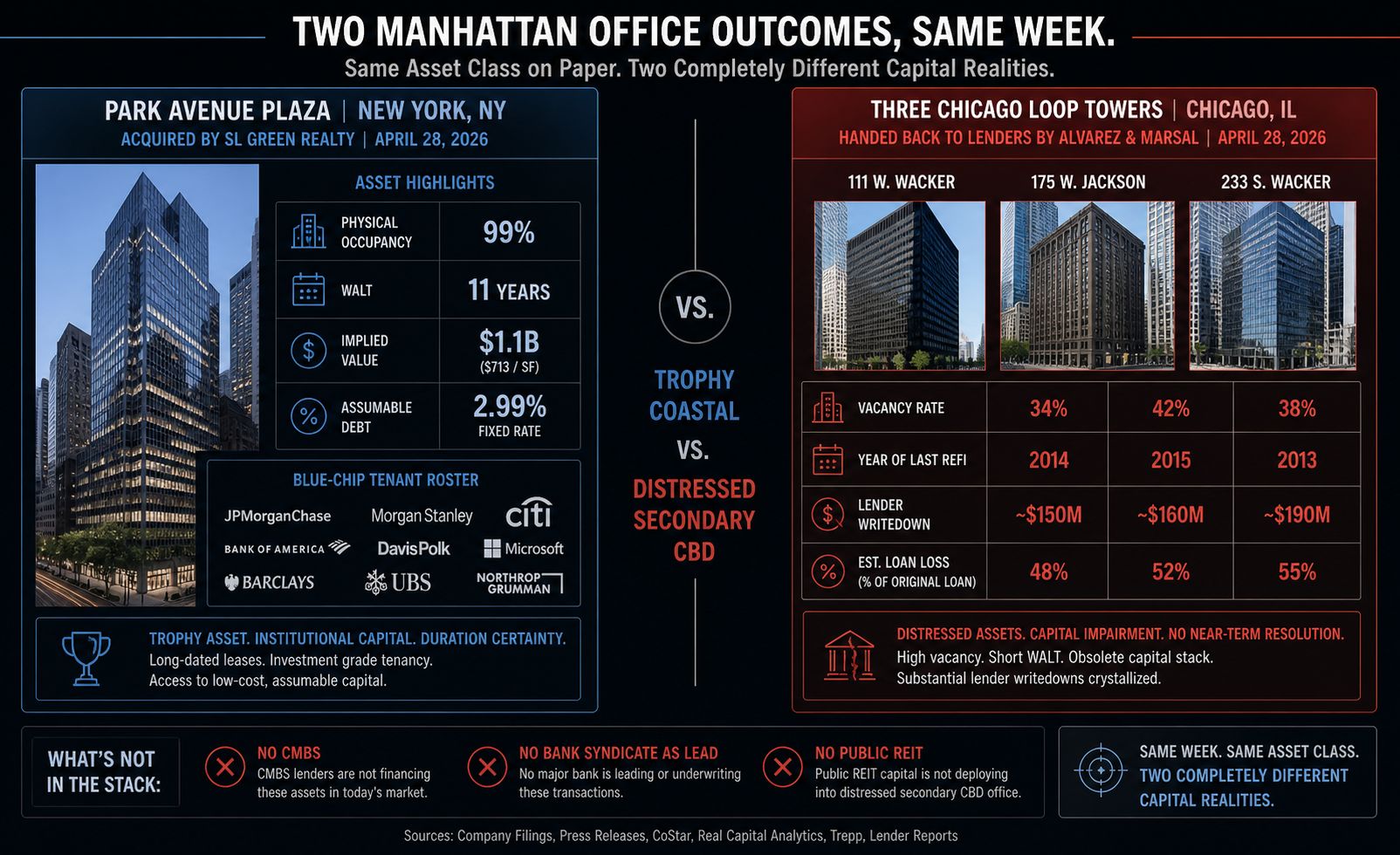

A major public REIT just paid up for a partial-interest position in a trophy Manhattan tower at the same moment Alvarez & Marsal surrendered its third distressed Chicago Loop office in 30 days. Same asset class, same week, two completely different outcomes.

This deal isn't about Manhattan office sentiment — it's about three separate assets being acquired in one transaction. Asset one: the building itself, with a high-credit rent roll and 11-year duration. Asset two: below-market in-place rents that mark to market over the lease cycle. Asset three — and the one most coverage misses — a 2.99% fixed-rate loan locked in until late 2031. In a 6%+ rate environment, that legacy debt is worth real money on its own. Vornado is paying for all three at once and treating the financing as part of the underwritten yield.

Implications for CRE:

The bifurcation thesis is now empirically settled. Trophy Manhattan office trades at premium valuations to in-place income; Class B/C in secondary CBDs gets handed back to lenders. Same product type, different capital outcome — and the gap is widening, not closing.

Cheap legacy debt is a tradable asset. Any pre-2022 fixed-rate loan with five-plus years of remaining term is now part of the building's value, not just a liability. Watch for partial-interest transactions specifically structured to transfer assumable financing.

Partial-interest acquisitions become the trophy-office liquidity vehicle. Few buyers can write a $1B-plus check for a single Manhattan tower in 2026. JV recaps and partial-interest purchases let trophy buildings trade without forcing a full marketing process or triggering loan refinance.

Cluster strategies justify premium basis. Vornado paid for adjacency to 350 Park — operational density across a few blocks creates leasing leverage and tenant-retention advantages that don't show up in a single-building cap rate. The next wave of Manhattan office consolidation will be geographic, not asset-by-asset.

The cap rate signal for Class A NYC office is stabilizing — at the very top only. This trade tells you nothing about Class B Midtown, suburban office, or anything outside the top 5% of the NYC office stack. Don't extrapolate.

Subscribe to CRE 360 Signal™ Newsletter to Move Smarter in Today's CRE Market.

Subscribe to CRE 360 Signal™ Newsletter to Move Smarter in Today's CRE Market. Key Takeaways

- Trophy Manhattan office isn't recovering — it never broke. What's actually happening is the rest of the office stack is repricing downward while the top tier holds, and the spread between them is now wide enough to be the trade itself. Underwrite Class A and Class B as separate asset classes, not points on the same curve.

Never miss a Signal

Get the daily brief that busy CRE professionals rely on.