➤ SIGNAL

The largest single source of multifamily debt just got materially bigger. The structure, not the size, is the tell.

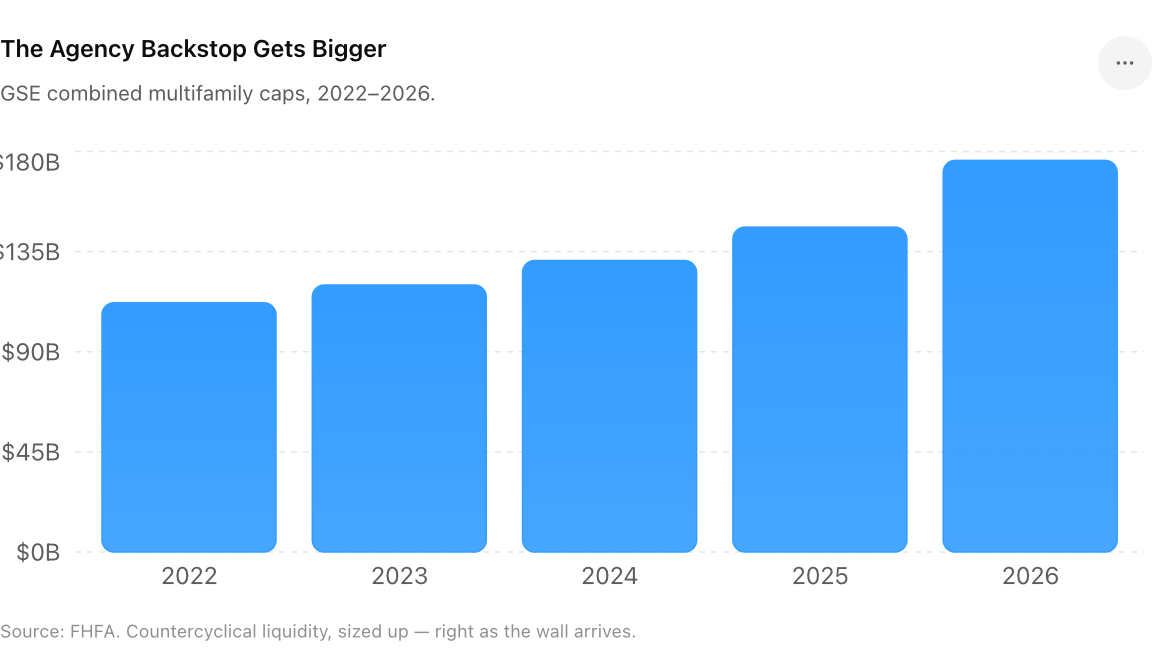

Agency lending is countercyclical liquidity — it expands precisely when private and bank capital pulls back. Raising the caps ~20% as the 2026 maturity wall crests is a deliberate liquidity backstop for the one asset class with the deepest public-policy support.

The mechanism that matters for underwriting: agency execution sets the floor on multifamily cap rates. A 20%-bigger cap means deeper, cheaper debt for qualifying product — and the qualifying gate is now explicitly affordable and workforce housing. The workforce-housing exclusion makes naturally-occurring affordable assets the single most financeable trade in the sector.

Market-rate luxury, especially in oversupplied Sun Belt submarkets, sits outside that lane and still competes for private and bank debt at wider spreads. The cap increase widens the gap between the financing cost of "mission" product and everything else.

Implications Two multifamily financing markets are forming. Workforce and affordable deals get an agency tailwind; luxury lease-up underwrites against a stuck 10-Year and tighter private credit.

Key Takeaways

- Agency capital just widened the on-ramp — but only for the deals Washington wants built.

Source: FHFA / Multifamily Dive / MBA — announced Nov 2025, effective 2026 · Policy · Multifamily · Capital Markets

Never miss a Signal

Get the daily brief that busy CRE professionals rely on.