➤ SIGNAL

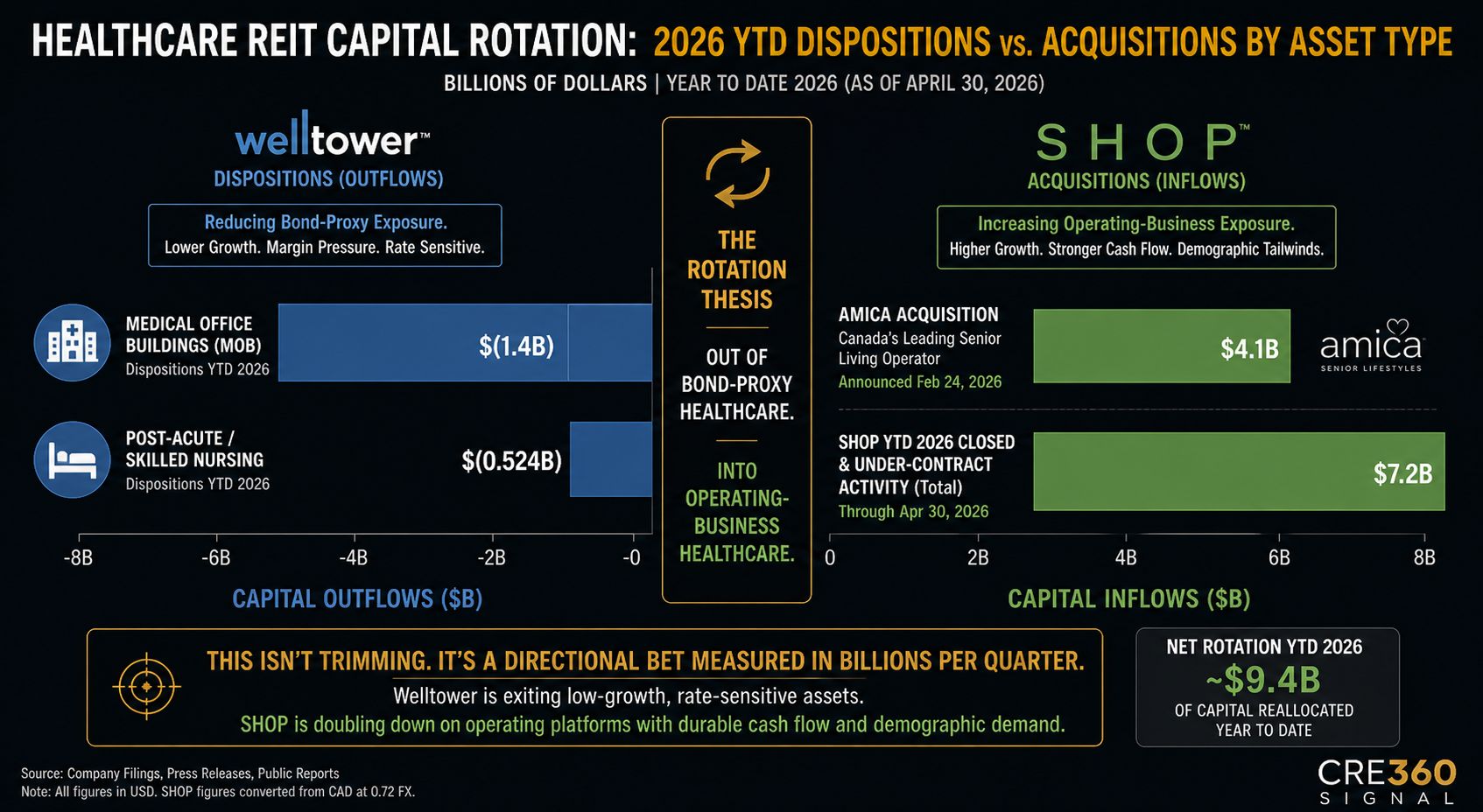

The largest healthcare REIT in the country is unloading medical office at scale into a market where private capital is paying up for it. That's not portfolio cleanup — that's a strategic call that MOB doesn't belong in the same vehicle as senior housing anymore.

Our angle: The market reads this as Welltower being bullish on senior housing. The sharper read is that Welltower is bearish on MOB at public-REIT cost of capital. MOBs trade like long-duration bonds — stable tenants, modest growth, low operating leverage. SHOP trades like an operating business — Boomer demographics, NOI growth in the mid-teens, real upside. A public REIT optimizing for FFO growth cannot justify holding both. Welltower picked the operating-business side and is funding it by selling the bond-proxy side to private buyers who actually want bond proxies.

Implications for CRE:

The MOB cap rate spread between public and private capital just widened structurally. Public REITs will continue selling; private buyers, family offices, and 1031 exchangers will continue paying. That spread is the trade for the next 18 months.

Healthpeak and Healthcare Realty face follow-on pressure. Once one major REIT signals MOB doesn't earn its cost of capital, the others either match the call or explain why they're different. Expect portfolio sales announcements within two quarters.

Senior housing development pipelines unfreeze. Welltower deploying $10.5B+ into SHOP at this pace pulls forward construction starts that have been stalled by interest rate uncertainty. Operator partners (Sunrise, Atria, Brookdale) get a capital partner with conviction.

The data-science licensing line is the under-covered angle. Welltower selling its operating platform to Public Storage means a healthcare REIT just monetized its tech stack across asset classes. That's a new revenue category for any REIT with proprietary operations infrastructure — and a competitive threat to vertical proptech vendors.

MOB underwriting needs to separate buyer types. Pro forma exit cap rates assuming "REIT bid" should be discounted; pro formas assuming private/family-office bid hold up. The buyer pool determines the basis, not the asset.

Subscribe to CRE 360 Signal™ Newsletter to Move Smarter in Today's CRE Market.

Subscribe to CRE 360 Signal™ Newsletter to Move Smarter in Today's CRE Market. Key Takeaways

- When the largest holder of a property type sells $1.4B of it in 90 days while private buyers pay premium prices for the same product, the asset class is being repriced by capital structure, not fundamentals. Underwrite MOB to the buyer who will actually own it at exit.

Never miss a Signal

Get the daily brief that busy CRE professionals rely on.