➤ SIGNAL

A franchisor announced a new economy extended-stay brand with $200M of committed development capital — the fourth such launch in 24 months alongside LivSmart by Hilton, Echo Suites by Wyndham, and StudioRes by Marriott. That alone would be a sector signal. The franchise-fee structure is what makes it a category event.

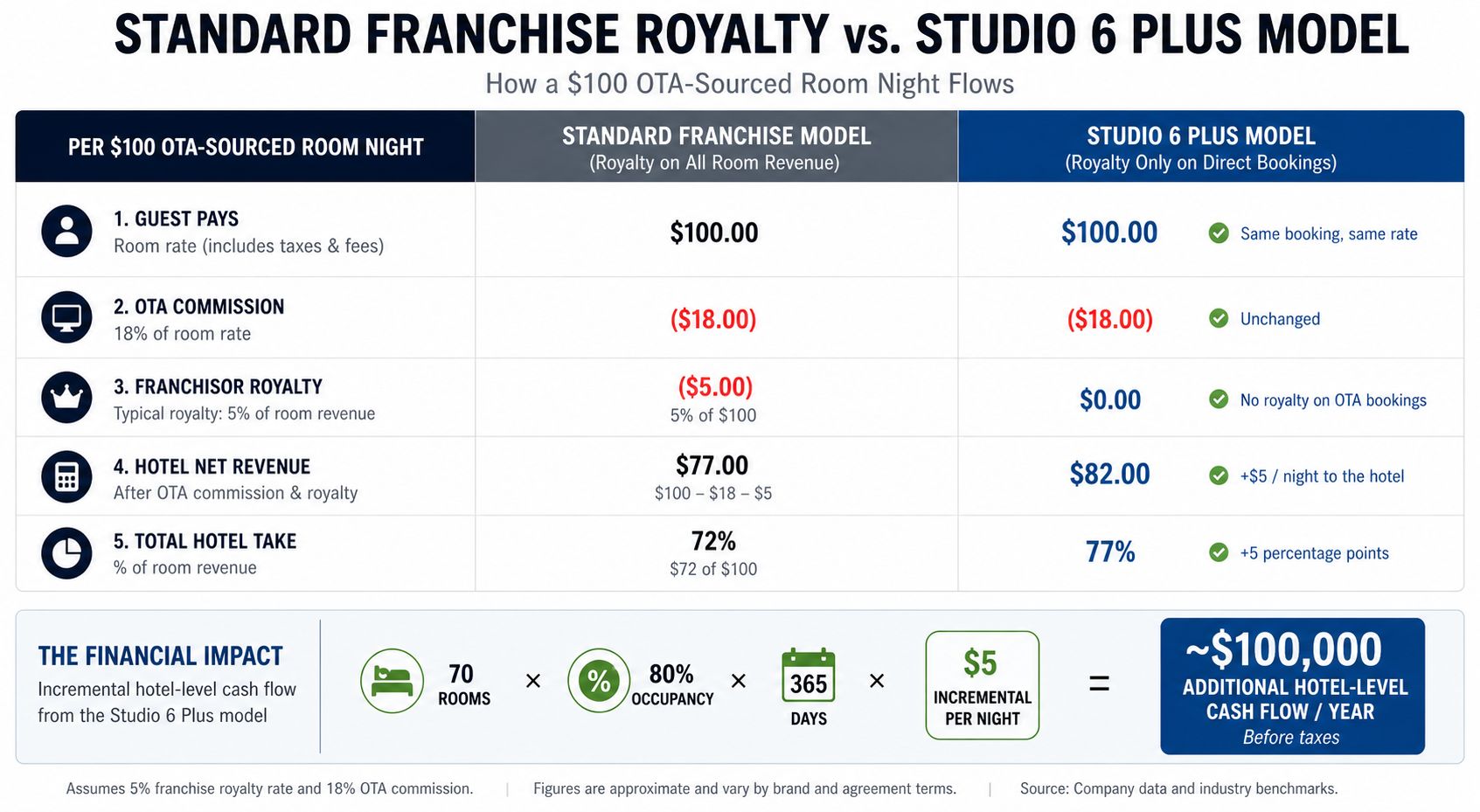

Our angle: Most coverage focused on the brand launch and the $200M Natson commitment. The underwriting story is the fee model. Standard franchisor economics charge royalties on total room revenue regardless of channel — meaning a hotel paying 15–25% commission to Expedia or Booking.com still owes the franchisor royalties on top of that haircut. G6 just told franchisees: we won't double-tax your OTA channel. If that catches on with even one Tier-1 franchisor, it rewrites the franchise pro-forma across the entire industry. If it doesn't, G6 still has a recruiting weapon that lets them out-compete on franchisee economics in the segment most exposed to OTA dependency.

Implications for CRE:

Economy extended-stay is now structurally oversupplied for the next 36 months. Four major brand launches in 24 months, all targeting the same labor-mobility tenant base, all underwriting to similar ADR/RevPAR bands. Older ES assets (Extended Stay America, WoodSpring, Candlewood pre-2018 vintage) in secondary markets where these prototypes will land face direct, branded, new-construction competition with materially lower operating costs.

The OTA fee carve-out forces a franchisor response. Hilton, Marriott, Wyndham, Choice, IHG cannot ignore this if Studio 6 Plus signs ten franchisees who would otherwise have signed with them. Expect quiet fee-structure adjustments at the franchise-agreement level — particularly for new-construction extended-stay deals — within four quarters.

Direct-booking share becomes a franchisee-recruiting metric, not just an operating metric. Operators who can demonstrate strong direct channels capture more of their own revenue under the G6 model. Brand websites, loyalty programs, and CRS investment now carry franchisee-economic implications, not just guest-experience ones.

Underwrite new ES construction to the prototype's ADR target, not the market's. Studio 6 Plus' $75–$90 ADR is a public floor for upper-economy ES new construction in 2026–2027. Pro formas pricing $110+ ADR in markets where Studio 6 Plus, LivSmart, or Echo Suites will land are pricing competition that hasn't arrived yet.

Existing ES owner-operators face a refinance problem before they face an operational one. Older vintage ES assets coming up on 2026–2027 maturities will be underwritten by lenders against the new prototype supply, not against the asset's last five years of performance. Cap rates widen on the older assets even before RevPAR moves.

Subscribe to CRE 360 Signal™ Newsletter to Move Smarter in Today's CRE Market.

Subscribe to CRE 360 Signal™ Newsletter to Move Smarter in Today's CRE Market. Key Takeaways

- A new economy ES brand alone wouldn't be a CRE signal. A new brand plus $200M committed plus a franchisor fee model that breaks twenty years of industry convention — that's the signal. Watch which franchisor copies the OTA carve-out first; that's the moment the model changes.

Never miss a Signal

Get the daily brief that busy CRE professionals rely on.