➤ SIGNAL

Supply discipline, not demand euphoria, is driving the squeeze: almost no new prime retail has been built in years.

Landlords have regained pricing power for the first time in nearly a decade.

The spread between prime corridors and secondary blocks keeps widening.

Manhattan retail spent 2017–2021 as the consensus short. The recovery has been grinding rather than dramatic — which is exactly why it has lasted. With availability at record lows and construction near zero, every incremental leasing decision now pressures rents.

The caution flag is the consumer: record-tight space against softening spending is a landlord's market with a fundamentals asterisk.

Implications

Retail underwriting in gateway corridors should now model rent growth, not just stabilization — but stress the tenant sales side.

Key Takeaways

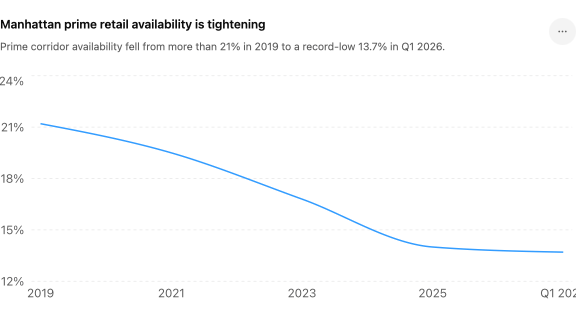

- Manhattan retail went from consensus short to supply-constrained in five years.

JLL Q1 2026 Manhattan Retail Report, via CoStar / CRE Daily / World Property Journal — published early June 2026 · Retail · Leasing · New York

Never miss a Signal

Get the daily brief that busy CRE professionals rely on.