➤ SIGNAL

The thesis is demographic and structural: care keeps migrating from hospitals to outpatient.

Buyers are paying for durable, needs-based tenancy — not a rate trade.

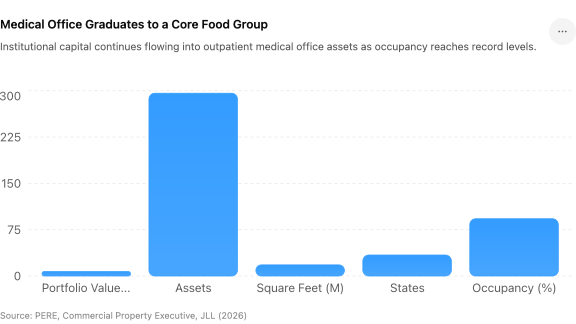

Medical outpatient buildings (MOBs) are being underwritten like the fifth major food group alongside office, industrial, retail, and multifamily. The portfolio scale here is the tell — this is institutional capital treating MOB as core, not niche.

Record occupancy in a year when most asset classes are still clearing excess space is the quiet headline. Healthcare tenancy is sticky: relocation is expensive, referral networks are local, and demand is non-discretionary.

The risk is paying core pricing for assets with hospital-system credit concentration or aging physical plant. Granularity matters — 296 assets across 34 states is a credit-and-condition diligence exercise, not a cap-rate exercise.

Implications Expect more aggregation plays. As capital eases, the next wave is roll-ups of fragmented MOB ownership into institutional-scale portfolios.

Key Takeaways

- When the safest rent in real estate is a doctor's lease, MOB stops being an alternative and becomes a core allocation.

PERE / Commercial Property Executive / JLL — closings through mid-2026

Never miss a Signal

Get the daily brief that busy CRE professionals rely on.