📢 CRE 360 Signal™.

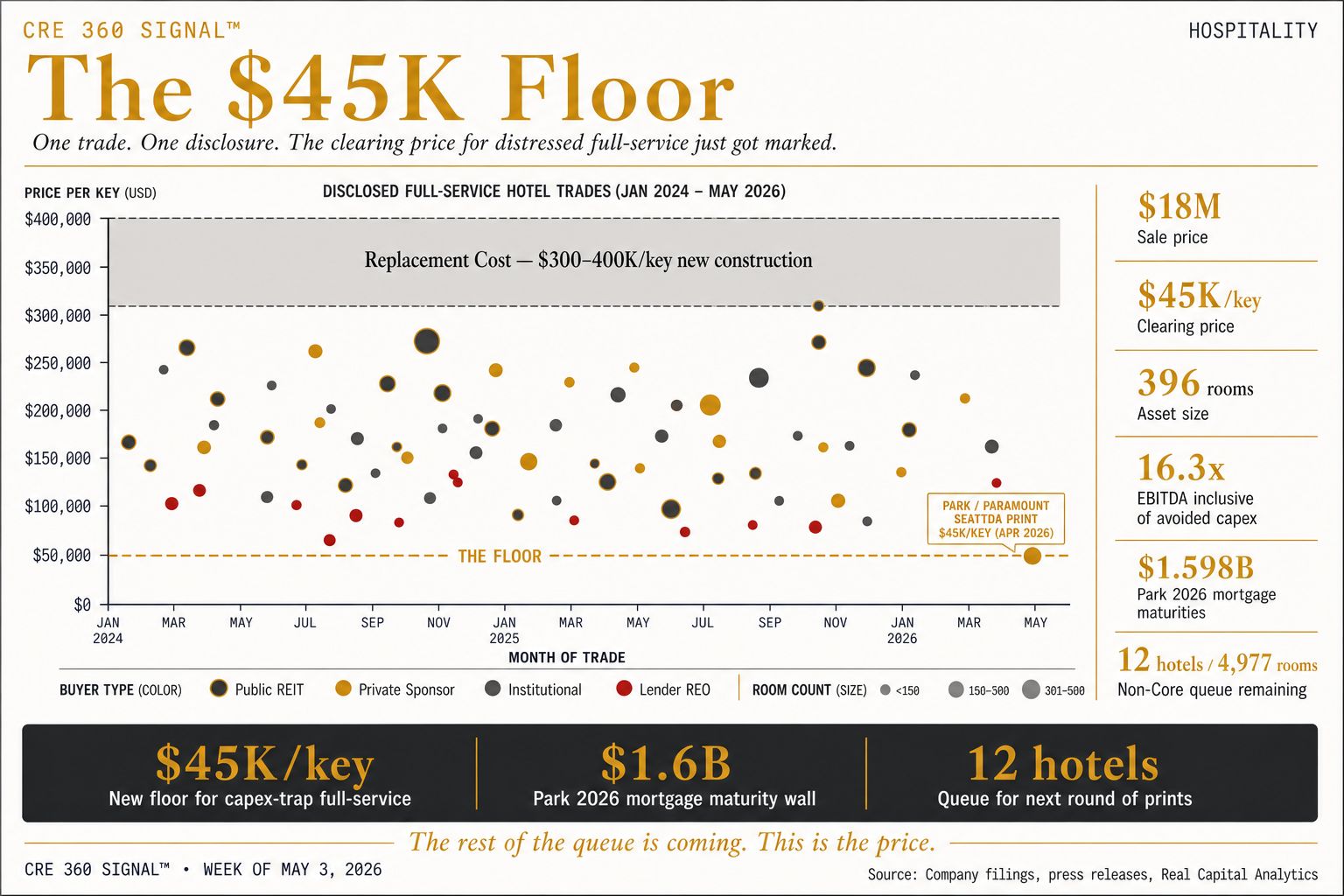

Park Hotels & Resorts sold the Hilton Seattle Airport for approximately $18 million — roughly $45,000 per key — and disclosed in the same Q1 release that $1.598 billion in mortgages mature throughout 2026. The trade isn't a strategic disposition. It's a benchmark print, and every lender, special servicer, and acquisition shop holding distressed full-service paper now has a defensible mark to reference.

🎧 Busy to read? Catch the Daily Podcast (Subscribe on YouTube, Apple, Spotify)➤ SIGNALS

Park Hotels & Resorts (NYSE: PK) disclosed in its April 30 Q1 release that it sold the 396-room Hilton Seattle Airport & Conference Center to a Bellevue-based affiliate of Paramount Hotels for approximately $18 million. The clearing price works out to roughly $45,000 per key. Combined with January's Hilton Checkers Los Angeles sale, year-to-date 2026 dispositions total about $31 million at 16.3 times 2025 EBITDA — a multiple Park is publicly framing as inclusive of avoided capex on the deferred renovations.

The buyer committed to a top-to-bottom renovation. That commitment is the deal — the seller priced out the capex Paramount is willing to absorb, and the multiple looks defensible only because the math credits the avoided PIP. Strip that out and the trade is closer to 8x on operating cash flow.

The same Q1 release disclosed $1.598 billion in mortgage loans maturing throughout 2026. Park's Non-Core program has 12 hotels remaining — 4,977 rooms generating $57 million in 2025 hotel-adjusted EBITDA. That's the queue for the next round of clearing prints, and the maturity wall is the forcing function.

Why It Matters

When a public REIT sells a full-service hotel for the cost of the renovation it was avoiding and discloses $1.6 billion in maturities the same day, the message isn't "strategic recycling" — it's "the rest of the queue is coming, and this is the price." Every special servicer holding distressed full-service paper, every lender marking CMBS positions, every acquisition shop underwriting capex-trap collateral — they all just got a public comp at $45,000 per key on a 396-room airport asset. The "EBITDA inclusive of avoided capex" framing becomes the standard, and sellers who can't credit avoided capex into the multiple are admitting the asset doesn't trade at a defensible going-concern cap rate.

Implications for CRE

$45K per key is the new floor for older-vintage, capex-trap, full-service hotels. Sellers pitching above that need to defend the gap with renovated condition, brand strength, or in-place income — not "comparable trades."

The public-seller / private-buyer dynamic is now the dominant hotel M&A trade. Local sponsors with renovation expertise and patient capital are the natural buyers; public REIT cost of capital can't justify holding the asset through a $30K per key PIP. Expect Pebblebrook, RLJ, Sunstone, and DiamondRock to follow with similar non-core prints.

The 12 remaining Park Non-Core hotels are a forward calendar. $57 million in 2025 EBITDA across 4,977 rooms gives you a rough sizing for the next round of prints. Watch for them quarter by quarter.

Lender behavior is the watch item. A $45K per key public comp gives every special servicer holding distressed full-service paper a defensible mark for note sales, discounted payoffs, and deed-in-lieu valuations. Expect a pickup in note-sale activity in 2026 H2.

Key Takeaways

When a public REIT sells a full-service hotel for the cost of the renovation it was avoiding and discloses $1.6 billion in maturities the same day, that's not strategic recycling. That's the floor being set. Underwrite full-service acquisitions to that floor — not to the seller's broker pitch.

CRE 360 Signal™ — Commercial Real Estate Intelligence

▼ EDITORIAL DESK TOP PICKS

🏢 Office / Leasing / Urban Markets

WTC district now rivals Midtown with $140+ rents — Downtown Manhattan leasing has surged, pushing rents above $100–$160 PSF with ~95% occupancy.

Office towers selling at up to 95% discounts — Distressed office assets across major cities are trading at fractions of prior values, signaling structural repricing.

Dallas office building sale tied to renovation strategy — A 115K SF office asset is being repositioned to Class A quality amid ongoing demand shifts.

⚡ Industrial / Data Centers

$2B data center expansion in Texas backed by Oracle demand — DataBank is scaling a 600K SF campus with 180 MW capacity, reflecting AI-driven infrastructure demand.

ICE warehouse acquisitions creating new CRE asset class — Federal purchases of industrial assets for detention facilities are reshaping warehouse demand and pricing.

🔗 https://www.wsj.com/business/logistics/ice-dhs-detention-center-warehouses-ac0af8e4

🏗️ Development / Mixed-Use / Adaptive Reuse

Dodgers stadium land seen as major CRE development opportunity — Large-scale mixed-use potential tied to transit infrastructure could unlock billions in value.

Oceanwide Plaza $470M deal faces financing and legal hurdles — One of LA’s largest stalled projects continues through bankruptcy with multiple bidders.💰 Capital Markets / Debt / Regulation

Fed examining banks’ exposure to private credit funds — Regulators are concerned about growing links between banks and nonbank CRE lending structures.

Private credit exposure flagged as “growing and opaque” — CRE lending risk is increasingly shifting outside traditional banking channels.

🏢 Brokerage / Industry Structure

Re/Max to be acquired in ~$880M deal — Consolidation continues as tech-enabled brokerages scale nationally.

🌍 Market Trends / Investment Signals

CRE increasingly tied to AI and tech infrastructure demand — Data centers are becoming one of the fastest-growing asset classes globally.

95% of investors planning increased data center allocation — Institutional capital is aggressively shifting toward digital infrastructure.

Office leasing showing early recovery signals in multiple markets — Positive absorption is spreading across U.S. metros despite elevated vacancy.

Luxury retail expansion up 65% year-over-year — High-end retail is outperforming due to resilient high-income consumers.

🏠 Housing / Multifamily / Spillover Effects

Housing slowdown creating buying opportunity for investors — Reduced competition and slower sales are improving acquisition conditions.

Mortgage rates stabilizing around 6.3%–6.5% range — Elevated but predictable rates are shaping acquisition and development strategies.

🏦 Macro / Structural CRE Shifts

CRE debt market now exceeds $5 trillion — Banks still dominate but non-bank lenders continue gaining share.

Banks hold ~$1.89T of income-producing CRE loans — Traditional lenders remain core but are losing relative dominance.

🏬 Retail / Experiential / Distress

American Dream mall faces $800M debt dispute — Bondholders allege manipulation of property value amid financial stress.

Saks Fifth Avenue closing stores tied to CRE restructuring — Retail bankruptcies continue to reshape mall tenancy and valuation dynamics.

Get Park Hotels Just Set the Floor in your inbox

A 396-room Hilton sold for $45K per key the same week Park flagged $1.6B in 2026 mortgage maturities.