➤ SIGNAL

The scarcity is structural — almost no new retail has been built in a decade.

Grocery-anchored and high-income suburban corridors are the tightest.

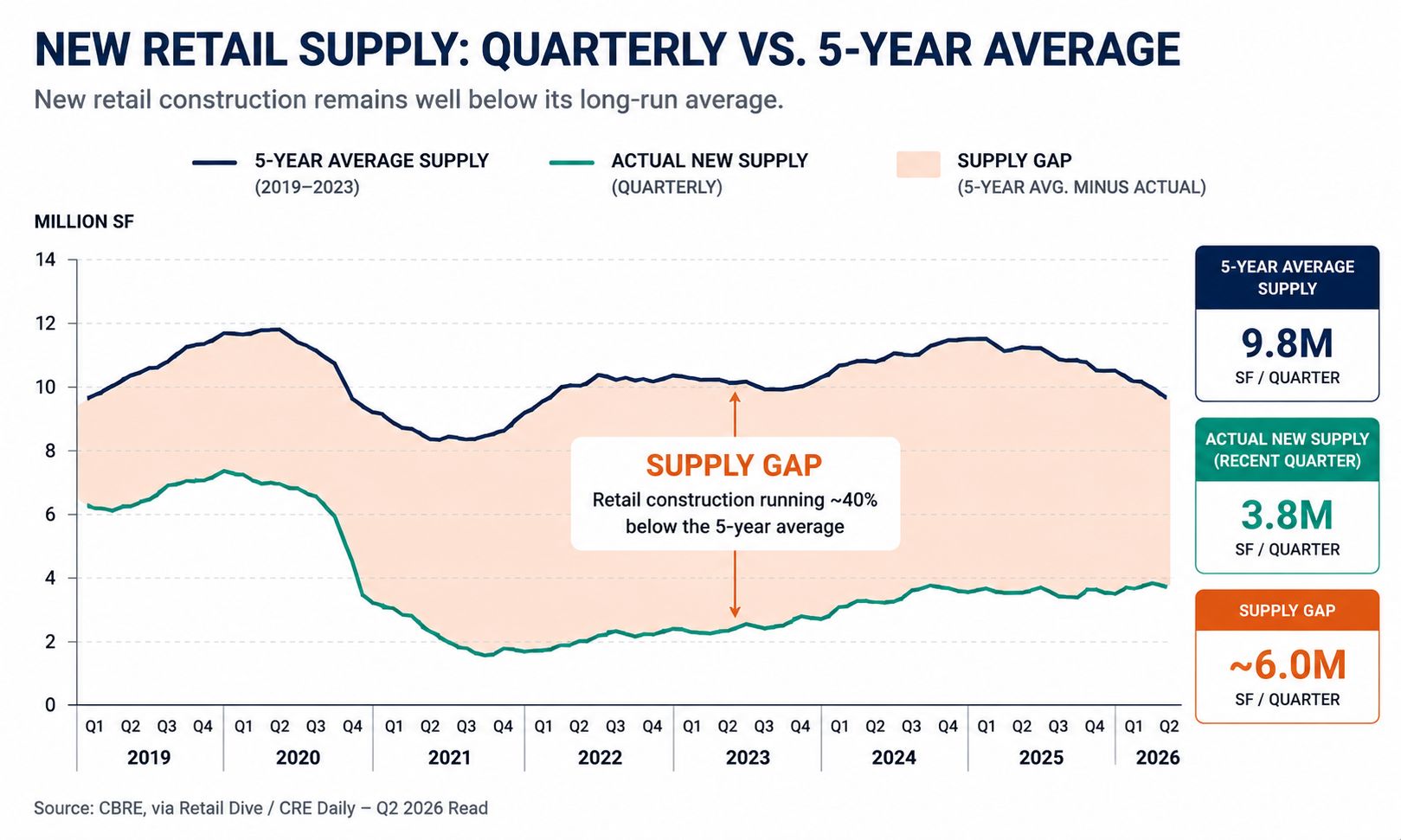

Retail flipped from the most-feared asset class to one of the tightest. The cause is supply, not a demand miracle: developers stopped building retail after 2010, and the existing stock is now absorbing a healthy consumer with nowhere new to go.

New supply at roughly 40% of the long-run average means landlords hold pricing power for the first time in years. That's why strip rents are rising while the headline narrative still treats retail as troubled.

The investment read is sale-leasebacks and net lease. With M&A reviving, more operators will monetize owned real estate, feeding single-tenant net-lease product into a supply-starved market.

Implications Underwrite retail on irreplaceability, not nostalgia. Grocery-anchored centers in supply-locked corridors are the durable trade; commodity power centers are not.

Key Takeaways

- A decade of building nothing turned retail into a landlord's market — scarcity, not foot traffic, is the story.

CBRE, via Retail Dive / CRE Daily — recent Q2 2026 read

Never miss a Signal

Get the daily brief that busy CRE professionals rely on.