➤ SIGNAL

A pure capital-markets advisory shop is being absorbed into a full-service global platform.

The acquirer paid to buy distribution and relationships at the top of the market.

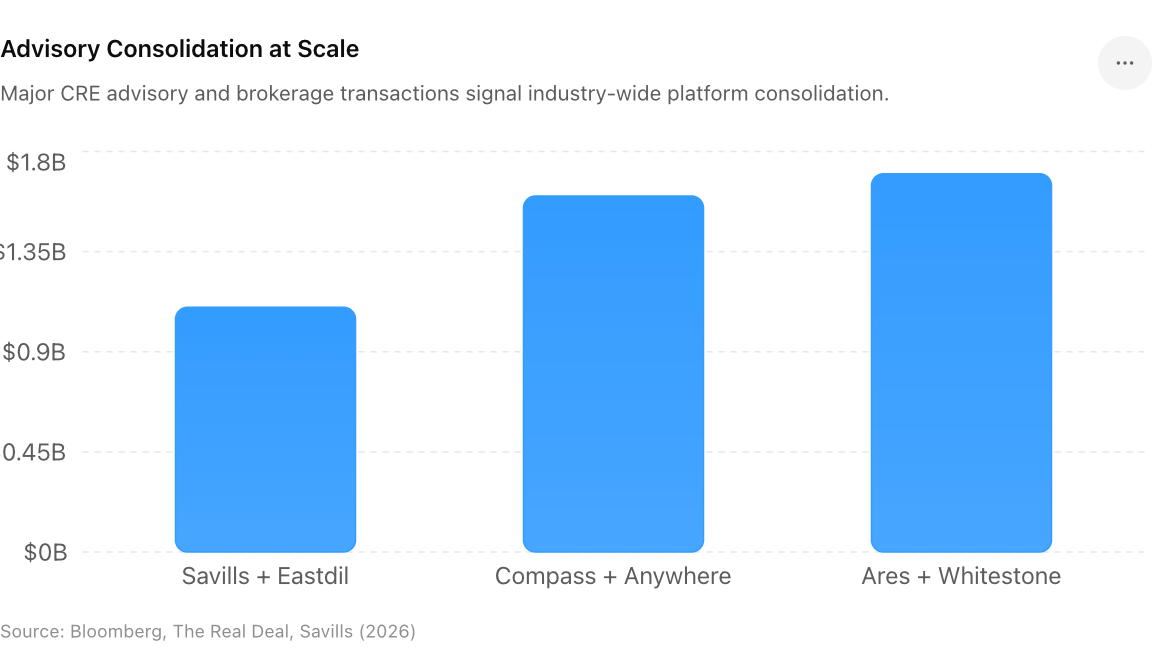

Consolidation is now visible across brokerage, advisory, and investment management simultaneously.

Eastdil is the most concentrated franchise in large-deal capital markets advisory. Buying it is buying a Rolodex and a profit-share culture that has historically been hard to replicate. Savills kept both the name and the comp structure precisely because the people are the asset.

The wider read is structural. When transaction volume is uneven, scale and service breadth become defensive. Advisors are consolidating to capture larger mandates, cross-sell leasing and management, and spread fixed cost across more revenue lines. The flag here is timing — announced in March — but the consolidation thesis is very much a live 2026 story.

Implications For clients, fewer independent top-tier advisors means relationship and conflict management get harder on the largest deals. For mid-market shops, the gap to the top widens — niche specialization or local depth becomes the only defensible lane.

Key Takeaways

- At the top of the market, advisory is consolidating into platforms — and independence is becoming the scarce commodity.

Bloomberg / The Real Deal / Savills

Never miss a Signal

Get the daily brief that busy CRE professionals rely on.