📢Good morning,

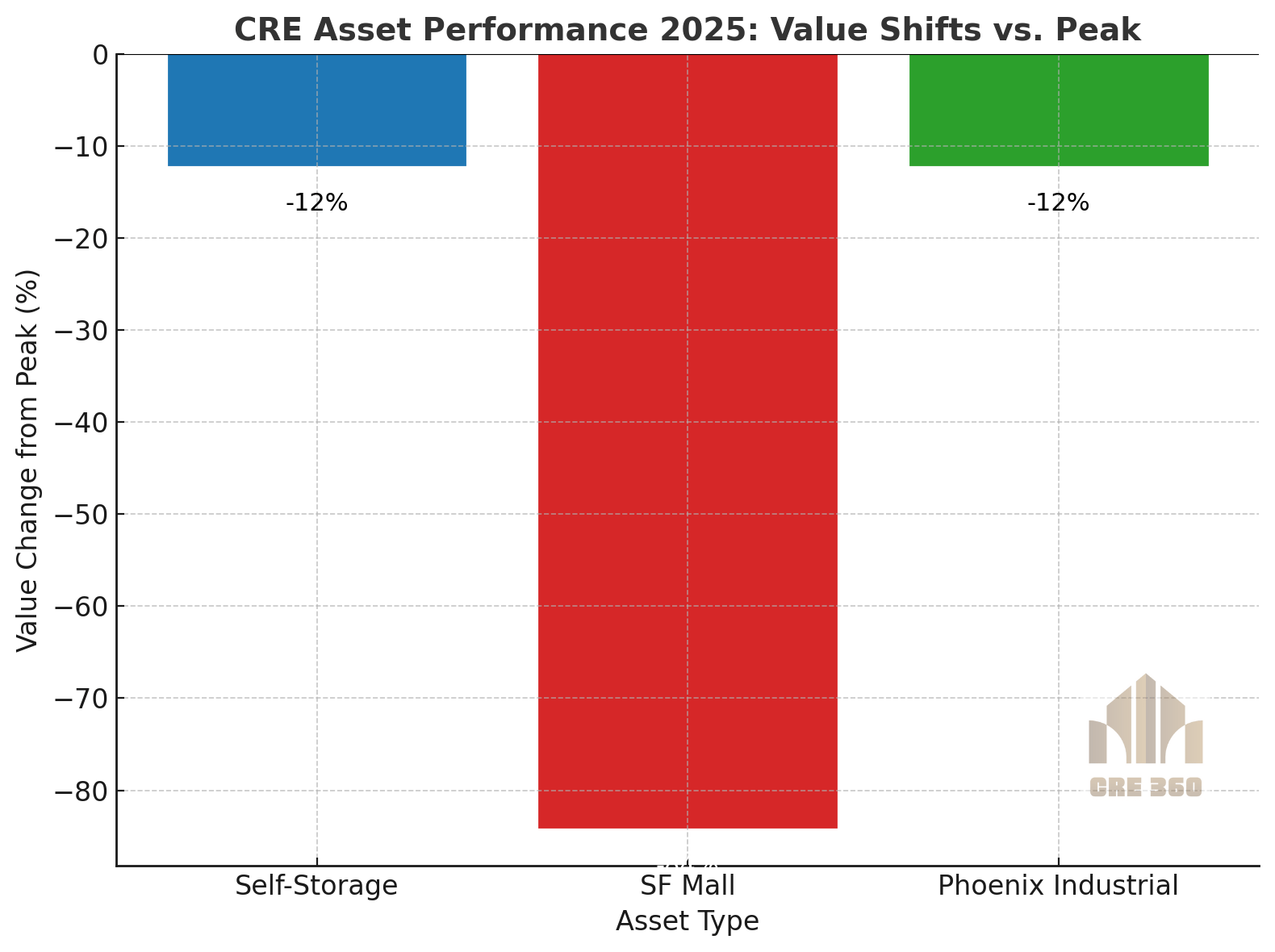

The self-storage sector is finding its footing after years of pandemic-fueled expansion. Average property values dipped about 12% from the Q1 2023 peak ($174/SF → $159/SF), but transaction volume held at $2.85B in H1 2025, essentially back to pre-2020 levels. Occupancy remains high near 90%, with asking rents steady at $128/unit/month. Cap rates have leveled off at ~5.8%, confirming investor confidence. Unlike offices and malls, storage continues to prove itself as a durable, recession-resistant niche.

📊 Quick Dive

Transaction volume: $2.85B in H1 2025 — matching 2019 levels (CRE Direct).

Cap rates: ~5.8%, up modestly from the 5.0% pandemic lows (Trepp).

Occupancy: ~90% nationwide, with 10.5% of U.S. households renting units (Yardi).

San Francisco Flagship Mall Value Collapses 80%

The 1.5M SF San Francisco Centre Mall, formerly Westfield, has been reappraised at just $195M, an 84% drop from its ~$1.2B valuation in 2016. Occupancy has plummeted to 7% after Nordstrom and Bloomingdale’s closures, leaving the property nearly vacant. With $626M in outstanding debt, foreclosure is imminent. This marks one of the most dramatic mall devaluations in U.S. history and highlights the growing “urban retail doom loop” in cities grappling with remote work, e-commerce, and declining foot traffic.

Phoenix Industrial Portfolio Trades for $168M with 80% Leverage

BKM Capital Partners acquired 889K SF across 8 industrial parks in Phoenix and Tempe for $167.8M (~$189/SF), financed with 80% loan-to-cost debt. The portfolio was ~90% occupied at closing, underscoring strong tenant demand for small-bay industrial. While metro Phoenix has 17.4M SF under construction, absorption turned positive in Q2 2025, and vacancy ticked down to ~11%. Lender willingness to fund at such high leverage highlights industrial’s continued resilience compared to other CRE sectors.

Self-storage’s resilience is a reminder that not all CRE sectors move in lockstep. While office and retail face structural headwinds, storage and industrial continue to show income durability. Investors should focus on stable cash-flow assets with modest but predictable growth, particularly in niches like storage, last-mile logistics, and necessity-driven real estate.

For operators, the key is discipline: underwrite conservatively, avoid chasing yesterday’s growth, and prioritize retention. Lenders are rewarding stabilized income streams. In today’s bifurcated market, defense is the best offense — lean into assets that already perform rather than betting on distressed repositionings without clear exit strategies.

Retail resets: Expect more urban mall foreclosures in 2025–26, with lenders taking control at 50–80% discounts.

Industrial resilience: Phoenix and similar growth markets will remain favored, though supply absorption is key to watch.

Storage equilibrium: With new supply slowing, storage fundamentals should remain stable into 2026, supporting continued liquidity.

Capital flight-to-quality: Debt and equity will continue prioritizing resilient, income-producing asset classes over speculative repositioning.

Self-Storage: –12% (resilient, stabilizing), SF Mall: –84% (collapse), Phoenix Industrial: –12% (holding strong with leverage confidence)

Get 🟡Self-Storage Market Stabilizes in 2025 in your inbox

Pandemic boom cools into a steady, resilient asset class.