➤ SIGNAL

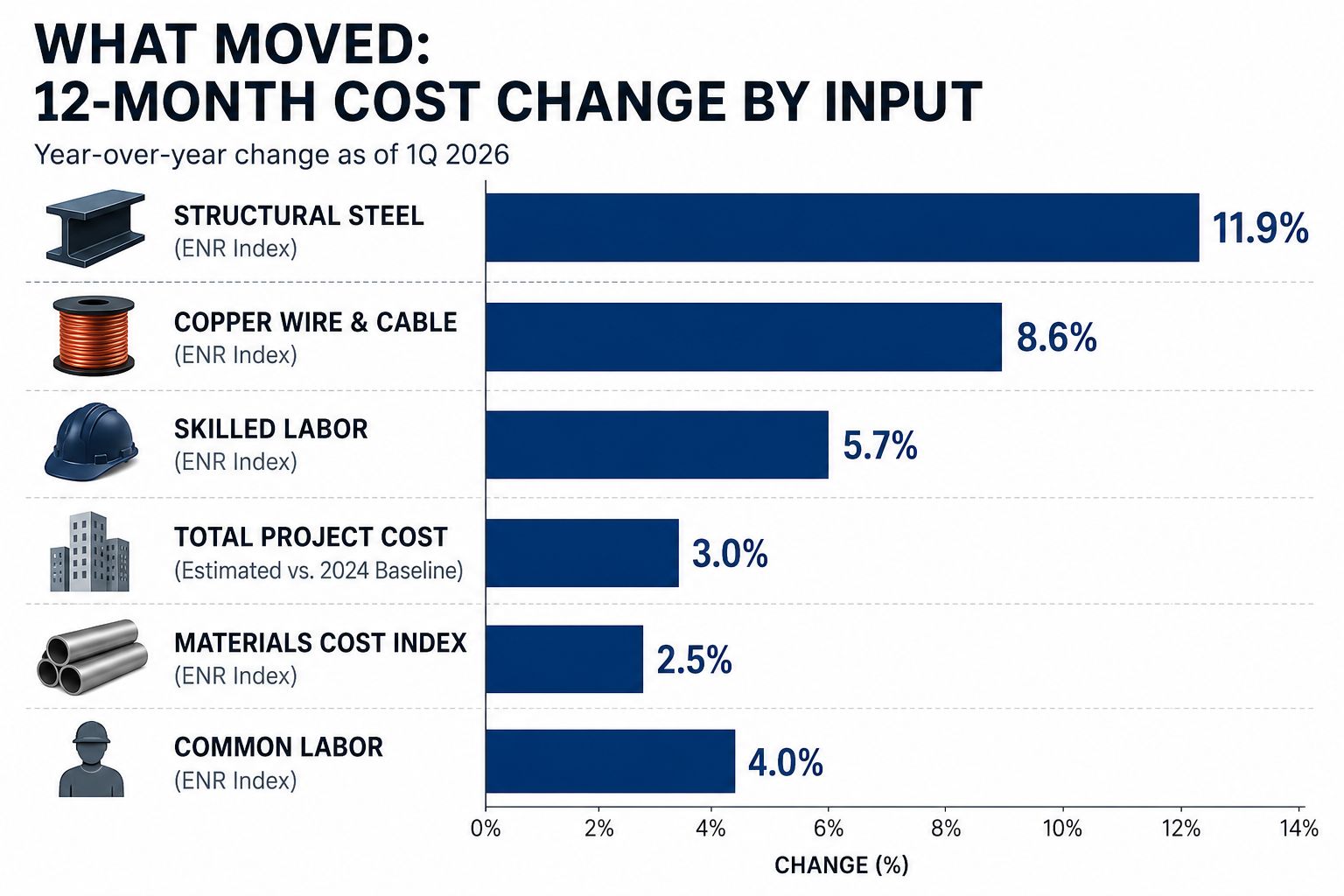

The hit is concentrated in steel, copper wire, cable, and industrial controls — the spine of any structure.

A 3% bump to total project cost is a margin event on a thin development spread.

This is a basis reset, not a blip. Every deal still penciling on 2024 hard-cost assumptions is now underwater on contingency before the first shovel.

The damage is uneven by product. Steel- and copper-heavy programs — industrial, data centers, mid- and high-rise — absorb the most. Wood-frame, garden-style product is more insulated.

The second-order effect is restraint. When replacement cost jumps, marginal new supply doesn't get built — which is bullish for existing, well-located assets and helps explain why sectors like retail (Signal 4) stay tight.

For owners and developers, the move is procurement discipline: lock pricing early, escalate contingency, and treat material escalation as an underwriting line item, not a footnote.

Implications Higher replacement cost is a tax on new development and a quiet subsidy to in-place assets. Expect more sale-leasebacks and acquisitions of standing product over ground-up starts.

Key Takeaways

- When it costs 3% more to build the same building, the cheapest square foot is the one that already exists.

Engineering News-Record 1Q 2026 Cost Report & Construction Economics (Jun 1, 2026) / Construction Dive

Never miss a Signal

Get the daily brief that busy CRE professionals rely on.