📢 CRE 360 Signal™.

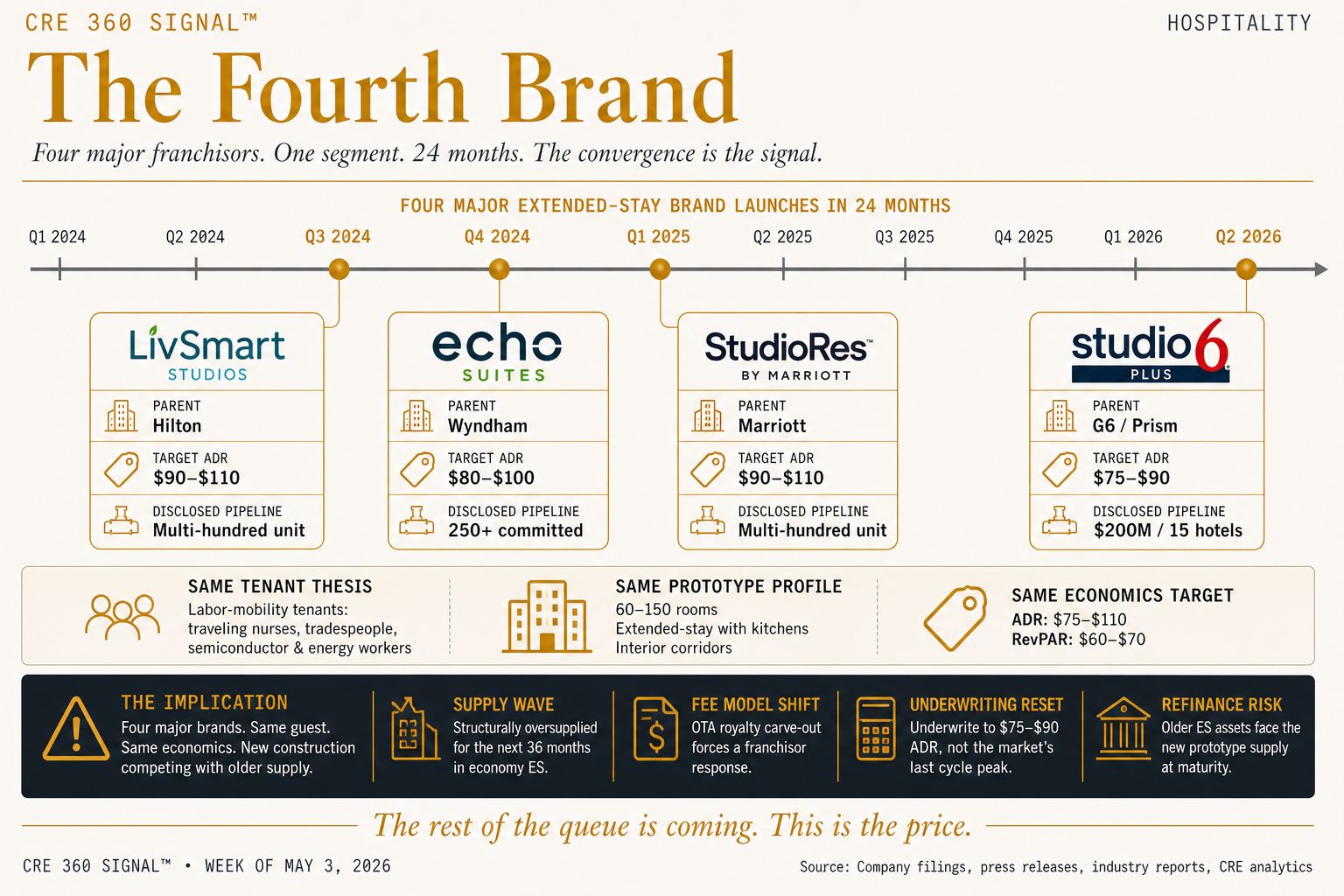

G6 Hospitality launched Studio 6 Plus on April 29 with Atlanta-based Natson Hotel Group committing approximately $200 million to develop the first 15 properties. The brand launch is the headline. The franchise-fee structure — royalties charged only on direct bookings, not on OTA-sourced revenue — is the category event that pressures every major franchisor's economics for the first time in twenty years.

🎧 Busy to read? Catch the Daily Podcast (Subscribe on YouTube, Apple, Spotify)➤ SIGNALS

At its franchisee convention in Cancún, G6 Hospitality (parent: India's Prism/OYO; CEO Sonal Sinha) unveiled Studio 6 Plus, an upper-economy extended-stay prototype targeting 60 to 150 rooms with full kitchens, interior corridors, and a target ADR of $75 to $90 with RevPAR of $60 to $70. Natson Hotel Group, based in McDonough, Georgia, committed roughly $200 million to develop the first 15 properties. The demand thesis is the same labor-mobility tenant base driving the broader extended-stay supply wave: traveling nurses, tradespeople, semiconductor and energy project workers.

The brand itself is the fourth major economy-to-upper-economy extended-stay launch in 24 months, alongside LivSmart by Hilton, Echo Suites by Wyndham, and StudioRes by Marriott. Even as the overall U.S. hotel construction pipeline contracted roughly 5% YoY in Q1 2026, the extended-stay segment continues to absorb new capital at a pace that disconnects from the rest of the industry.

The structural break is the fee model. Standard franchisor economics charge royalties on total room revenue regardless of distribution channel — meaning a hotel paying 15% to 25% commission to Expedia or Booking.com still owes the franchisor royalties on top of that haircut. G6 told franchisees it will charge fees only on direct bookings. The OTA channel runs without the franchise royalty layered on top.

A new economy extended-stay brand alone wouldn't be a CRE signal — there are already three of them. A new brand plus $200 million committed plus a franchisor fee model that breaks twenty years of industry convention is a different category of event. If the OTA carve-out catches on with even one Tier-1 franchisor, it rewrites the franchise pro-forma across the entire industry. Hilton, Marriott, Wyndham, Choice, and IHG cannot ignore this if Studio 6 Plus signs ten franchisees who would otherwise have signed with them. Direct-booking share — historically a guest-experience and marketing metric — now becomes a franchisee-recruiting metric and a hotel-level economic differentiator.

Implications for CRE

Economy extended-stay is now structurally oversupplied for the next 36 months. Four major brand launches in 24 months, all targeting the same labor-mobility tenant base, all underwriting to similar ADR and RevPAR bands. Older ES assets — Extended Stay America, WoodSpring, Candlewood pre-2018 vintage — in secondary markets where these prototypes will land face direct, branded, new-construction competition with materially lower operating costs.

The OTA carve-out forces a franchisor response. Expect quiet fee-structure adjustments at the franchise-agreement level — particularly for new-construction extended-stay deals — within four quarters. Franchisor M&A pressure increases as the smaller brands lose their fee-economics advantage.

Underwrite new ES construction to the prototype's ADR target, not the market's. Studio 6 Plus' $75 to $90 ADR is a public floor for upper-economy ES new construction in 2026 to 2027. Pro-formas pricing $110-plus ADR in markets where Studio 6 Plus, LivSmart, or Echo Suites will land are pricing competition that hasn't arrived yet.

Existing ES owners face a refinance problem before they face an operational one. Older-vintage ES assets coming up on 2026 to 2027 maturities will be underwritten by lenders against the new prototype supply, not against the asset's last five years of performance. Cap rates widen on the older assets even before RevPAR moves.

Key Takeaways

A new economy ES brand wouldn't move the underwriting model. A new brand with a franchise fee structure that breaks two decades of industry convention is the signal. Watch which Tier-1 franchisor copies the OTA carve-out first — that's the moment the model changes for everyone.

CRE 360 Signal™ — Commercial Real Estate Intelligence

▼ EDITORIAL DESK TOP PICKS

🏢 Office / Leasing / Urban Markets

WTC district now rivals Midtown with $140+ rents — Downtown Manhattan leasing has surged, pushing rents above $100–$160 PSF with ~95% occupancy.

Office towers selling at up to 95% discounts — Distressed office assets across major cities are trading at fractions of prior values, signaling structural repricing.

Dallas office building sale tied to renovation strategy — A 115K SF office asset is being repositioned to Class A quality amid ongoing demand shifts.

⚡ Industrial / Data Centers

$2B data center expansion in Texas backed by Oracle demand — DataBank is scaling a 600K SF campus with 180 MW capacity, reflecting AI-driven infrastructure demand.

ICE warehouse acquisitions creating new CRE asset class — Federal purchases of industrial assets for detention facilities are reshaping warehouse demand and pricing.

🔗 https://www.wsj.com/business/logistics/ice-dhs-detention-center-warehouses-ac0af8e4

🏗️ Development / Mixed-Use / Adaptive Reuse

Dodgers stadium land seen as major CRE development opportunity — Large-scale mixed-use potential tied to transit infrastructure could unlock billions in value.

Oceanwide Plaza $470M deal faces financing and legal hurdles — One of LA’s largest stalled projects continues through bankruptcy with multiple bidders.💰 Capital Markets / Debt / Regulation

Fed examining banks’ exposure to private credit funds — Regulators are concerned about growing links between banks and nonbank CRE lending structures.

Private credit exposure flagged as “growing and opaque” — CRE lending risk is increasingly shifting outside traditional banking channels.

🏢 Brokerage / Industry Structure

Re/Max to be acquired in ~$880M deal — Consolidation continues as tech-enabled brokerages scale nationally.

🌍 Market Trends / Investment Signals

CRE increasingly tied to AI and tech infrastructure demand — Data centers are becoming one of the fastest-growing asset classes globally.

95% of investors planning increased data center allocation — Institutional capital is aggressively shifting toward digital infrastructure.

Office leasing showing early recovery signals in multiple markets — Positive absorption is spreading across U.S. metros despite elevated vacancy.

Luxury retail expansion up 65% year-over-year — High-end retail is outperforming due to resilient high-income consumers.

🏠 Housing / Multifamily / Spillover Effects

Housing slowdown creating buying opportunity for investors — Reduced competition and slower sales are improving acquisition conditions.

Mortgage rates stabilizing around 6.3%–6.5% range — Elevated but predictable rates are shaping acquisition and development strategies.

🏦 Macro / Structural CRE Shifts

CRE debt market now exceeds $5 trillion — Banks still dominate but non-bank lenders continue gaining share.

Banks hold ~$1.89T of income-producing CRE loans — Traditional lenders remain core but are losing relative dominance.

🏬 Retail / Experiential / Distress

American Dream mall faces $800M debt dispute — Bondholders allege manipulation of property value amid financial stress.

Saks Fifth Avenue closing stores tied to CRE restructuring — Retail bankruptcies continue to reshape mall tenancy and valuation dynamics.

Get The Franchise Model Just Cracked in your inbox

G6 Hospitality launched Studio 6 Plus with $200M committed and a no-OTA-fee structure that pressures every franchisor's economics.