➤ SIGNAL

Demand didn't disappear; it got selective.

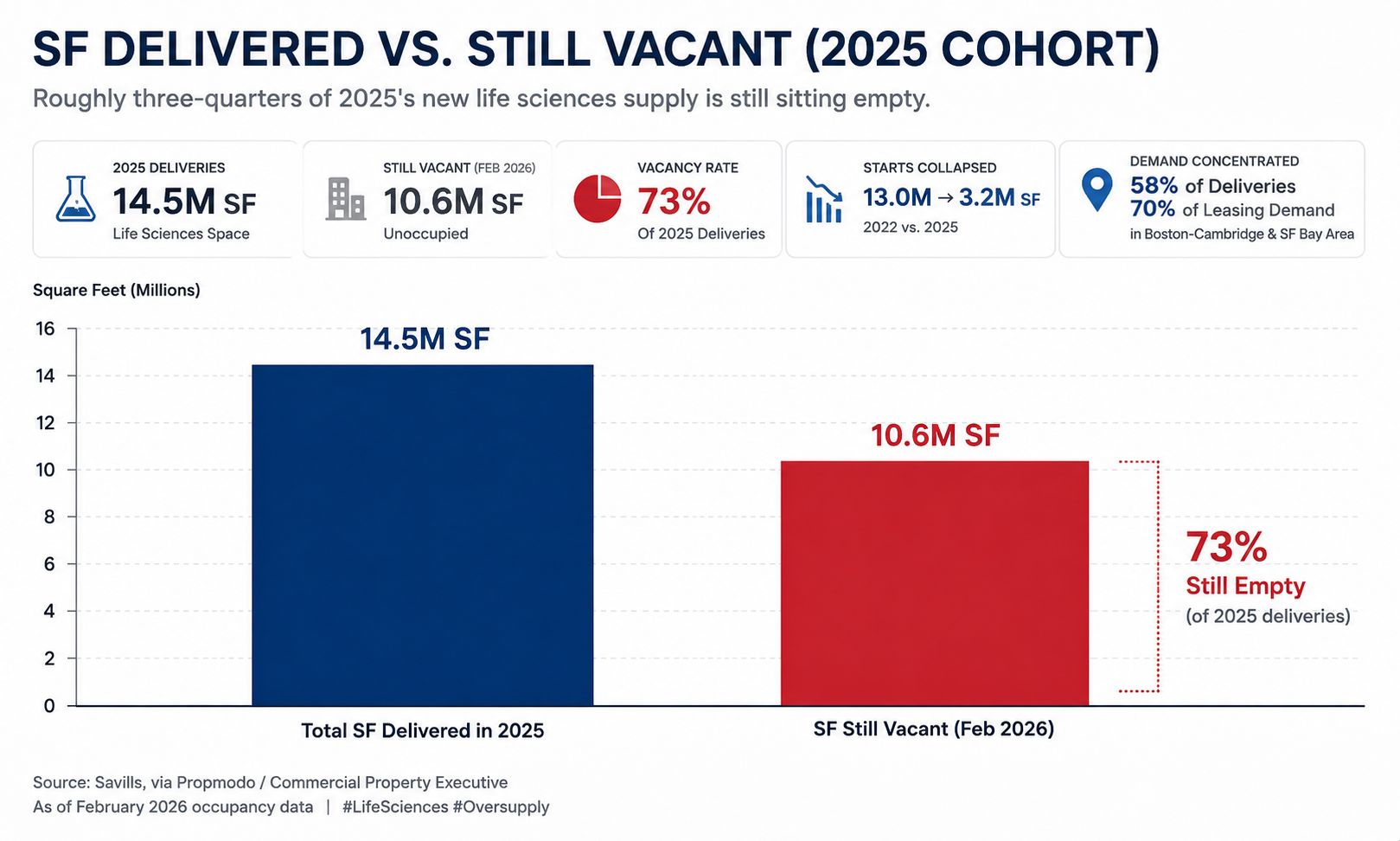

The boom was underwritten on a tenant base that never arrived at the assumed velocity.

The story isn't a demand collapse — it's a supply overshoot meeting a pickier tenant. Developers built to a 2021 absorption curve and delivered into a 2025 funding environment. Tenants now have optionality they didn't have three years ago, and they're using it.

Sublease space is widening the discount, giving growth-stage biotech a cheap path into trophy buildings. That helps tenants and punishes the marginal landlord who financed at peak.

The concentration cuts both ways. Boston and the Bay carry the demand, but they also carry most of the empty square footage. A national "life sciences" vacancy number hides two very different markets underneath it.

For underwriting, the lesson is old and expensive: specialized product with a thin tenant universe is the first to gap out when the cycle turns. Lab fit-out is hard to repurpose, so the downside is structural, not cosmetic.

Implications The repricing is coming through rent concessions and sublease discounts first, valuations second. Watch the gap between trophy and commodity lab space — it will widen the way it did in office.

Key Takeaways

- Life sciences proved the rule: specialized supply built on a single cycle's demand curve is the first to break when the curve flattens.

Savills, via Propmodo / Commercial Property Executive — as-of Feb 2026 occupancy data

Never miss a Signal

Get the daily brief that busy CRE professionals rely on.