➤ SIGNAL

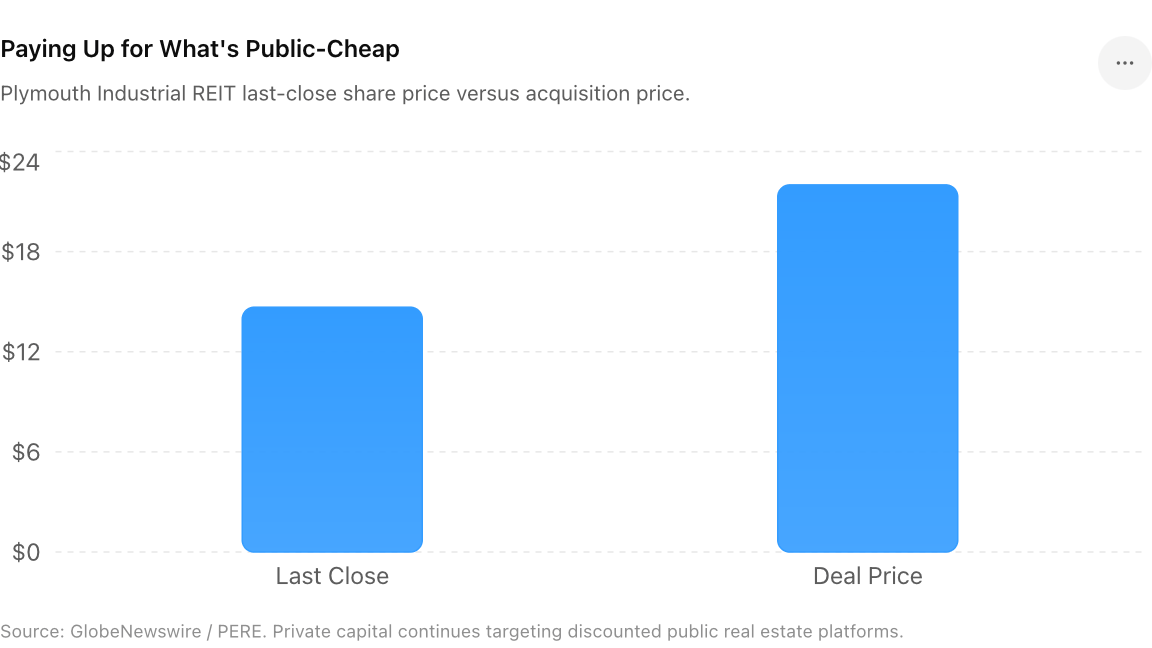

A ~50% premium is the headline number — it prices the gap between where public markets value stabilized industrial and where private capital will underwrite it. When credit-oriented buyers pay up for hard assets, read the spread, not the deal.

That a 2024-vintage structured-capital shop and a major alternative-credit manager will pay half again over the tape for an industrial portfolio says the public REIT was trading below replacement cost and below private NAV. That is the arbitrage of this cycle, executed in cash.

Implications Expect more take-privates in beaten-down public sectors — industrial and multifamily platforms first — while private capital sits on record dry powder and a stuck 10-Year keeps public REITs cheap. Public REIT boards now face a binary: close the NAV discount or get taken out.

Key Takeaways

- When private buyers pay 50% over the tape, the public market is the one that's mispriced.

- Source line: PERE / GlobeNewswire / Connect CRE — closed Jan 27, 2026 · Industrial · M&A · Public-to-Private

Never miss a Signal

Get the daily brief that busy CRE professionals rely on.