📢 CRE 360 Signal™.

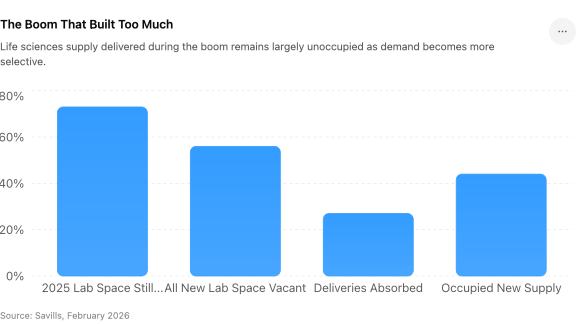

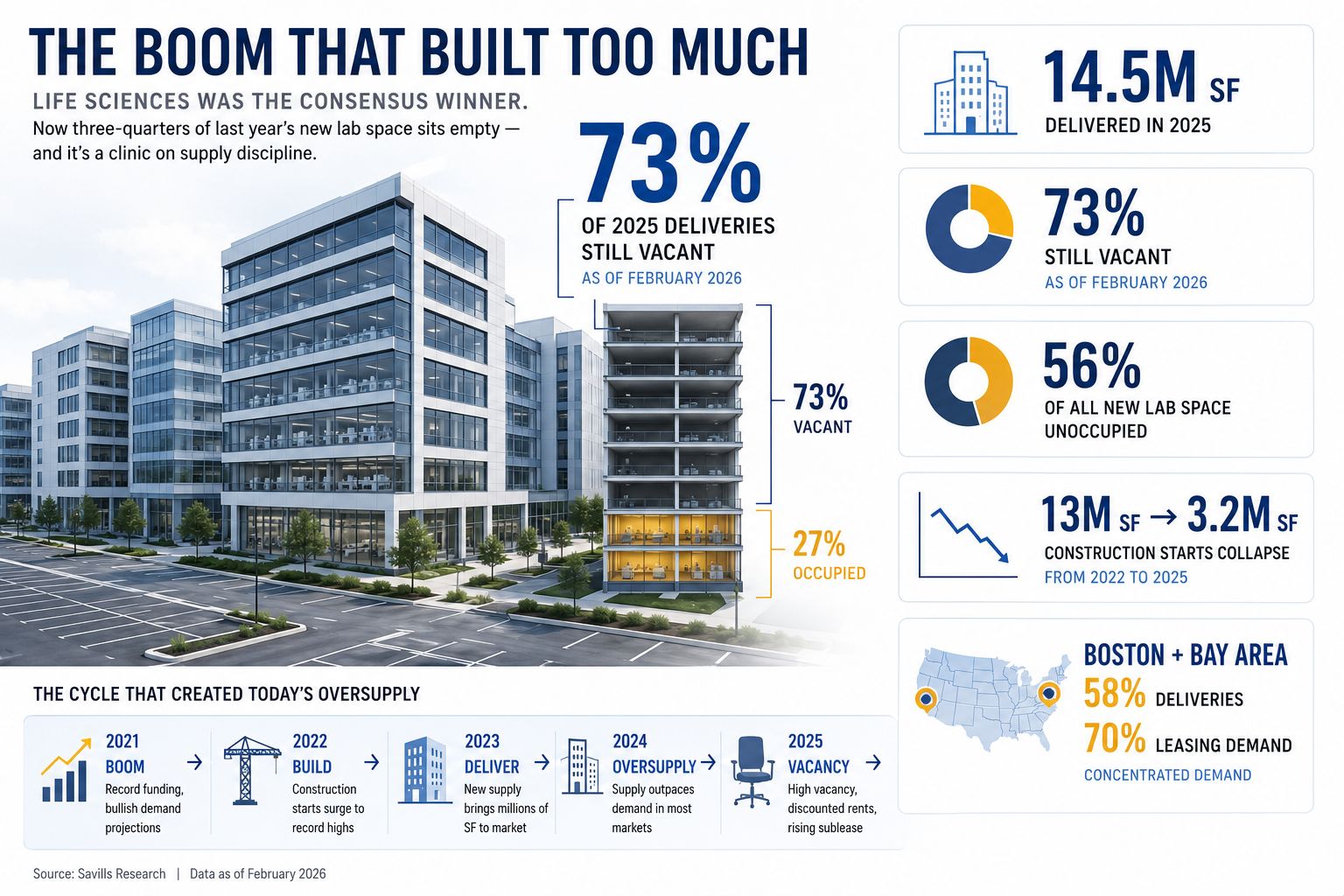

The most-hyped property trade of the last cycle is now its clearest cautionary tale. Roughly 73% of the 14.5 million square feet of life sciences space delivered in 2025 was still vacant as of February 2026, per Savills — and about 56% of all newly delivered lab space sits unoccupied. This is what a supply overshoot looks like when it finally meets the market.

🎧 Catch the Wekkly Podcast (Subscribe on YouTube, Apple, Spotify)➤ SIGNALS

The numbers describe an overshoot, not a collapse. Construction starts have already fallen hard — from roughly 13 million square feet in 2022 to about 3.2 million in 2025 — as the pipeline corrects. But the space built during the boom is still working through the system, and tenants are in no hurry.

Demand is concentrated and selective. Boston-Cambridge and the San Francisco Bay Area absorbed roughly 58% of recent deliveries and about 70% of leasing demand. The strongest tenants now have options — and a growing pool of discounted sublease space — so they're negotiating, not chasing.

Implications

This is a textbook lesson in underwriting specialized product. Lab space is among the most expensive square footage to build and the hardest to repurpose. When demand for highly specific product is underwritten on a single cycle's absorption curve, the downside isn't a soft patch — it's structural vacancy that can't be cured by dropping the rent on a generic floor plan.

The repricing will arrive in sequence: concessions and sublease discounts first, then headline rents, then valuations. The marginal landlord — the one who financed a speculative lab build at peak basis — is the exposed party. The institutional owner with leased, well-located product in a primary cluster is relatively insulated.

It also exposes the danger of a national average. A single "life sciences vacancy" figure blends a demand-rich Cambridge with a glutted secondary market. The real intelligence is in the submarket and the building, not the sector label — and the spread between trophy and commodity lab space is about to widen the way it did in office.

The broader read connects to the rest of today's package. Life sciences overbuilt; retail (a decade of building almost nothing) is now the tightest it's been in 20 years; data centers can't build fast enough because power, not capital, is the wall. The common thread isn't rates — it's supply discipline. In 2026, the asset classes winning and losing are sorted almost entirely by who got the supply curve right.

Stakeholder lens. Developers: stress-test specialized product against a thin tenant universe before committing capital to non-repurposable fit-out. Lenders: watch lab construction loans underwritten in 2021–2022 — the collateral is harder to re-tenant than a comparable office. Investors: the discount is real, but distinguish discounted-trophy (a buying opportunity) from cheap-and-stranded (a value trap).

Key Takeaways

Key Takeaway. Life sciences didn't lose its demand — it lost its discipline. The space built to a 2021 thesis is the bill coming due, and the only durable hedge is underwriting specialized supply to the tenant base that actually exists.

CRE 360 Signal™ — Commercial Real Estate Intelligence

▼ EDITORIAL DESK TOP PICKS

1. Commercial Real Estate Lending Activity Reaches Five-Year High. CBRE's Lending Momentum Index reached its strongest level since 2021, signaling increased lending activity across CRE sectors.

2. Commercial & Multifamily Borrowing Increased 52% in Q1 2026. MBA reported commercial and multifamily mortgage borrowing rose 52% year-over-year in the first quarter.

3. Kayne Anderson Closes $5.12 Billion Opportunistic Real Estate Fund. The firm announced the final close of an oversubscribed opportunistic equity fund with $5.12 billion in commitments.

4. CMBS Special Servicing Rate Reaches 11%. Trepp data shows the CMBS special servicing rate climbed to approximately 11% in May.

5. FDIC Reports Rising Nonperforming Commercial Real Estate Loans. The FDIC's Q1 banking report showed continued deterioration in nonfarm nonresidential CRE credit performance.

6. I Squared Acquires Data Center Portfolio From Cogent. I Squared Capital agreed to acquire U.S. data center assets from Cogent for approximately $225 million.

7. Edged Secures Nearly $2 Billion for U.S. Data Center Expansion. Edged announced approximately $2 billion in financing to support its U.S. data center development pipeline.

8. Prime Data Centers Breaks Ground on $3 Billion Phoenix Campus. Prime Data Centers started construction on three buildings within its $3 billion Metro Phoenix development.

9. PJM Accelerates Timeline for New Data Center Power Connections. PJM announced changes designed to speed up power delivery to large-scale data center projects.

10. AI Could Add 330 Million Square Feet of CRE Demand. Cushman & Wakefield projects AI-related growth could generate 330 million square feet of demand over the next decade.

11. JLL Arranges $300 Million Sale of FedEx Industrial Portfolio. A multi-state FedEx logistics portfolio traded for approximately $300 million.

12. Colliers Brokers $140 Million Industrial Facility Sale. A 1.6 million-square-foot industrial property in Tennessee sold for $140 million.

13. Newmark Arranges Sale and Financing of Logistics Portfolio. Newmark completed the sale and acquisition financing of a 1.38 million-square-foot shallow-bay logistics portfolio.

14. Industrial Asset in Northern Virginia Data Center Corridor Sells for $42 Million. Marcus & Millichap closed the sale of two industrial properties located within Northern Virginia's data center market.

15. ACRE Provides $351 Million Refinance for Multifamily Portfolio. ACRE supplied refinancing for a multifamily portfolio spanning four states.

16. HUD Expands Role in Multifamily Finance. HUD announced updates designed to increase its participation in multifamily lending programs.

17. Freddie Mac Issues Affordable Housing Forward Commitment. Freddie Mac provided a forward commitment supporting the development of new affordable housing in Arizona.

18. Avison Young Arranges $404 Million Permanent Loan in Manhattan. The firm secured financing for The Archive, a 479-unit multifamily property in Manhattan.

19. U.S. Office Vacancy Falls to 17.6%. Yardi Matrix reported national office vacancy declined modestly in April 2026.

20. Law Firms Continue Driving Premium Office Leasing. Savills reported legal-sector tenants remain among the most active users of high-end office space.

Key Takeaways

Still unresolved: Whether the 2025–2026 construction pullback is deep enough to let demand catch up by 2027, and how much of the standing vacancy is functionally obsolete versus simply early. The occupancy figures cited are as-of early 2026; the absorption trend through year-end is the number to watch.

Get The Boom That Built Too Much in your inbox

Life sciences was the consensus winner. Now three-quarters of last year's new lab space sits empty — and it's a clinic on supply discipline.