📢 CRE 360 Signal™.

Private capital is betting against public markets, paying premiums for commercial real estate, particularly in stabilized industrial, multifamily, senior housing, and supply-constrained infill sectors. This suggests a disconnect between public market valuations and private market assessments of value.

🎧 Catch the Wekkly Podcast (Subscribe on YouTube, Apple, Spotify)➤ SIGNALS

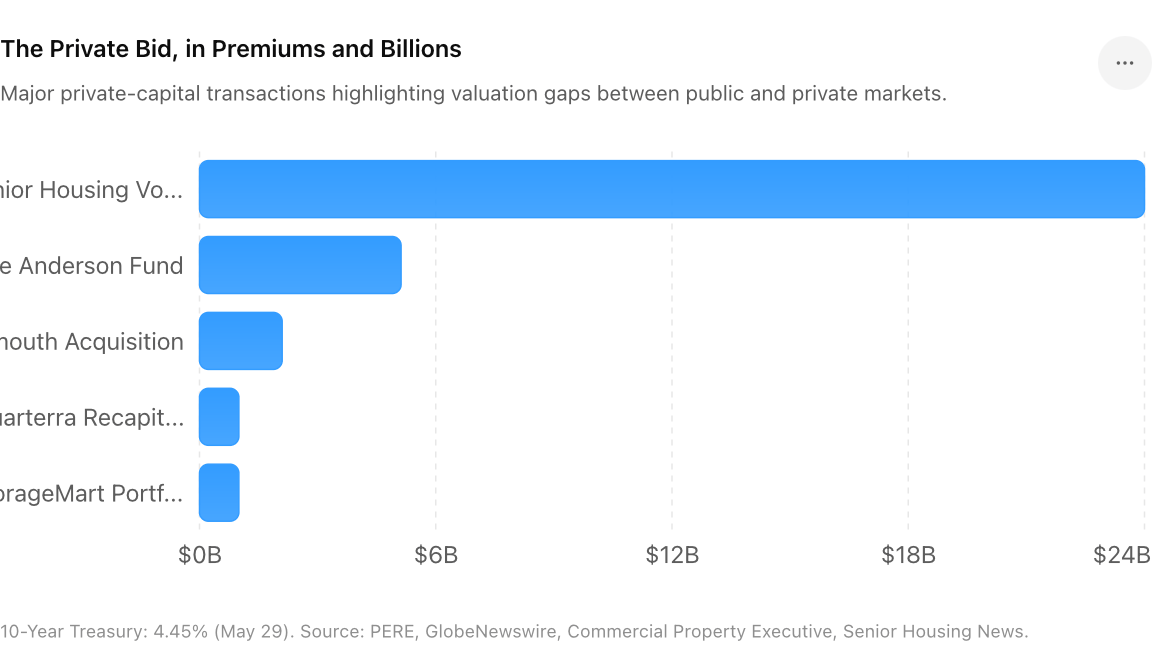

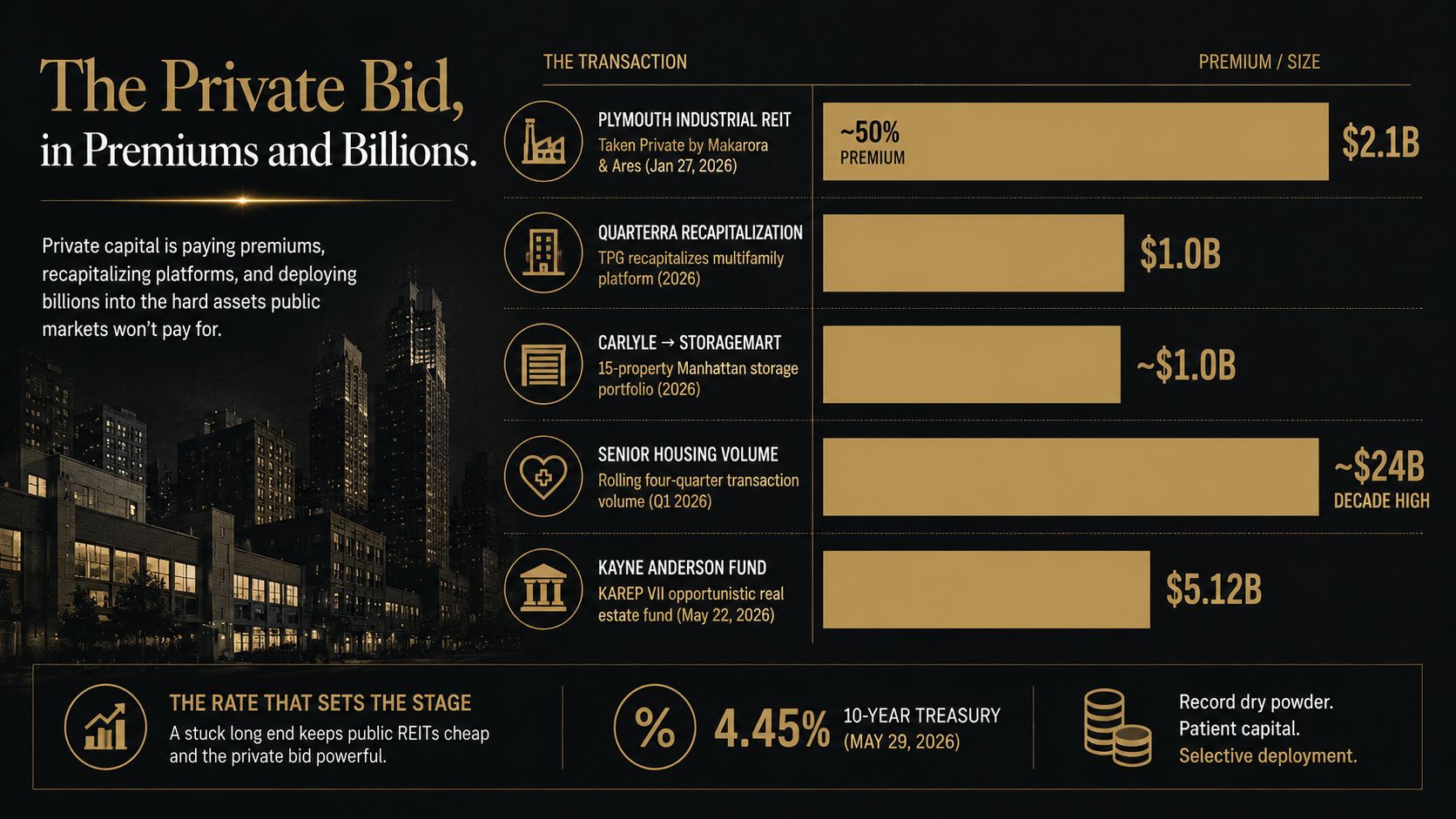

The clearest data point of the year so far is a premium. When Makarora and Ares took Plymouth Industrial REIT private in an all-cash deal this winter, they paid roughly 50% over the last public close — about $2.1 billion, at $22.00 a share, beating out a rival bid from Sixth Street. The company is gone from the exchange. The number that matters isn't the price; it's the spread between what the public market said stabilized industrial was worth and what private capital would actually underwrite.

It is not an isolated trade. TPG put roughly $1 billion into recapitalizing the multifamily platform Quarterra. Kayne Anderson closed its largest-ever opportunistic fund at $5.12 billion, with senior housing in the crosshairs. Carlyle sold a 15-property Manhattan self-storage book to StorageMart for about $1 billion. Senior-housing transaction volume hit a decade-high ~$24 billion. Different sectors, same signature: private buyers deploying into hard assets at prices the public tape wouldn't print.

All of it is happening against a 10-Year Treasury stuck at 4.45% (May 29) — the rate that prices fixed CRE debt, and the reason public REITs stay cheap.

Implications

The defining feature of this market isn't a crash; it's an arbitrage between the public and private read of the same buildings. Public REIT investors, marking to a daily tape and a stuck long end, are discounting hard assets below replacement cost. Private capital — sitting on record dry powder, with a longer hold and no quarterly mark — is exploiting the gap in cash.

But the bid is selective, and that selectivity is the whole story. It is flowing into stabilized industrial, multifamily platforms, senior housing, and supply-constrained infill — assets with durable, non-discretionary demand and a defensible basis. It is not indiscriminate. Commodity office, oversupplied Sun Belt storage, and luxury lease-up are not getting the call. This is the same dispersion the rest of the market is living, expressed as a buyer's checklist.

For public REIT boards, the math is now binary: close the NAV discount, or become someone's acquisition. A 50% premium is both a gift to current shareholders and an indictment of where the stock was trading. Expect the take-private list to grow while the long end stays put.

Key Takeaways

Public REIT boards: the discount is now a takeover invitation — address it or price it in. LP investors: the private bid is telling you where the durable-income trade is; follow the checklist, not the sector label. Lenders: a take-private at a 50% premium resets the comp set — your collateral may be worth more to a private buyer than to the tape. Owners weighing a sale: private capital is the deepest bid in the room for the right asset.

When private capital pays 50% over the public price for hard assets, the market that's mispriced is the one with a ticker.

CRE 360 Signal™ — Commercial Real Estate Intelligence

▼ EDITORIAL DESK TOP PICKS

1. Commercial Real Estate Lending Activity Reaches Five-Year High. CBRE's Lending Momentum Index reached its strongest level since 2021, signaling increased lending activity across CRE sectors.

2. Commercial & Multifamily Borrowing Increased 52% in Q1 2026. MBA reported commercial and multifamily mortgage borrowing rose 52% year-over-year in the first quarter.

3. Kayne Anderson Closes $5.12 Billion Opportunistic Real Estate Fund. The firm announced the final close of an oversubscribed opportunistic equity fund with $5.12 billion in commitments.

4. CMBS Special Servicing Rate Reaches 11%. Trepp data shows the CMBS special servicing rate climbed to approximately 11% in May.

5. FDIC Reports Rising Nonperforming Commercial Real Estate Loans. The FDIC's Q1 banking report showed continued deterioration in nonfarm nonresidential CRE credit performance.

6. I Squared Acquires Data Center Portfolio From Cogent. I Squared Capital agreed to acquire U.S. data center assets from Cogent for approximately $225 million.

7. Edged Secures Nearly $2 Billion for U.S. Data Center Expansion. Edged announced approximately $2 billion in financing to support its U.S. data center development pipeline.

8. Prime Data Centers Breaks Ground on $3 Billion Phoenix Campus. Prime Data Centers started construction on three buildings within its $3 billion Metro Phoenix development.

9. PJM Accelerates Timeline for New Data Center Power Connections. PJM announced changes designed to speed up power delivery to large-scale data center projects.

10. AI Could Add 330 Million Square Feet of CRE Demand. Cushman & Wakefield projects AI-related growth could generate 330 million square feet of demand over the next decade.

11. JLL Arranges $300 Million Sale of FedEx Industrial Portfolio. A multi-state FedEx logistics portfolio traded for approximately $300 million.

12. Colliers Brokers $140 Million Industrial Facility Sale. A 1.6 million-square-foot industrial property in Tennessee sold for $140 million.

13. Newmark Arranges Sale and Financing of Logistics Portfolio. Newmark completed the sale and acquisition financing of a 1.38 million-square-foot shallow-bay logistics portfolio.

14. Industrial Asset in Northern Virginia Data Center Corridor Sells for $42 Million. Marcus & Millichap closed the sale of two industrial properties located within Northern Virginia's data center market.

15. ACRE Provides $351 Million Refinance for Multifamily Portfolio. ACRE supplied refinancing for a multifamily portfolio spanning four states.

16. HUD Expands Role in Multifamily Finance. HUD announced updates designed to increase its participation in multifamily lending programs.

17. Freddie Mac Issues Affordable Housing Forward Commitment. Freddie Mac provided a forward commitment supporting the development of new affordable housing in Arizona.

18. Avison Young Arranges $404 Million Permanent Loan in Manhattan. The firm secured financing for The Archive, a 479-unit multifamily property in Manhattan.

19. U.S. Office Vacancy Falls to 17.6%. Yardi Matrix reported national office vacancy declined modestly in April 2026.

20. Law Firms Continue Driving Premium Office Leasing. Savills reported legal-sector tenants remain among the most active users of high-end office space.

Key Takeaways

Still unresolved: The arbitrage only persists while the public-private valuation gap stays open — which depends on the 10-Year. If the long end finally breaks below 4%, public REITs re-rate, the discount narrows, and the take-private window starts to close. Until then, the private bid is the marginal buyer setting price.

Get The Private Bid Comes Off the Sidelines in your inbox

Record dry powder is taking discounted REITs private and crowding into the assets public markets won't pay for.