Institutional Money Still Pays Up for the Grocery Run

Nuveen bought a fully-leased Chicago-suburb necessity center even as cap rates widen.

CRE360 Editorial Desk·Jul 14, 2026

U.S. markets, coast to coast

Nuveen bought a fully-leased Chicago-suburb necessity center even as cap rates widen.

Retail single-tenant yields rose to 6.60% in Q2 after the Fed dropped a 2026 cut from its projections.

Tenants signed 10.5M SF in Q2 and availability fell to its lowest since 2020.

Life-science tenants are re-leasing space fast, yet vacancy near 32% keeps rents falling.

Policy — not power supply — is now the variable reshaping digital-infrastructure underwriting.

A diversified select-service and extended-stay portfolio built around who fills the rooms.

A $42M SoCal lease and a 1.2M-sf Texas groundbreaking show occupiers committing long again.

Two summer trades and a decade-high preference reading show where cautious money is actually going.

Stargate Abilene crosses 1 GW as FERC forces grid operators to answer for hyperscale load.

2.7M SF of leases push occupancy to ~98% — including a 53-year ground lease in Hawaii.

Absorption climbs and prime vacancy falls — while commodity buildings still clear at 60–70% discounts.

Prologis posts record Q1 leasing and raises guidance as AI demand spills into industrial.

National Healthcare Properties exits stabilized medical office to double down on operating senior housing.

National multifamily is stabilizing on paper — but the Sun Belt is still correcting hard underneath.

AI was supposed to shrink legal footprints. In 2026 it's expanding them.

LA permitting jumps 85% while Sun Belt deliveries fall off a cliff.

A $32B sponsor consolidates its retail-heavy trust and sets a two-to-five-year listing clock.

Washington let the USMCA renewal deadline pass, converting a settled pact into an annual review.

UPDATE — National demand rebounds while the supply wave finishes clearing

Toronto-based owner confirms talks over a sale of "certain assets" from its 20M-SF book

Structural steel rose ~12% in a year as steel and aluminum tariffs doubled mid-cycle.

Q1 net absorption neared 40M SF — the strongest first quarter since 2023.

institutional capital, CRE debt markets, and the real‐asset risk stack — with real deployable capital flowing and practical enablers scaling with it.

AI workloads expose the limits of renewable-only energy strategies.

A massive Tesla battery marks a shift from grid expansion to real-time energy management.

Grid capacity and interconnection queues—not city plans—are deciding what gets built in 2026.

Public private-credit vehicles lag badly while large banks regain pricing power and execution advantage.

Capital is still available, but only for sponsors willing to reset basis and surrender leverage.

Loan extensions are expiring, forcing lenders to choose between restructuring, recapitalization, or exit.

Tariffs, outages, and tight inventories push copper into uncharted territory

Activist stake intensifies scrutiny as Target restructures leadership and capital priorities.

Here’s a quick look at how markets ended 2025 — with both stocks and precious metals pushing into rare territory.

Rezoning and phased planning frameworks establish certainty for large-scale residential infill development.

How the Chiefs and Lockton moves signal a structural shift in the Kansas City metro

Cities like Atlanta and Orlando show high return activity, with free shipping and at-home pickup emerging as key expectations.

60 new locations in 2026 and recent record openings underscore deliberate resource allocation across key markets.

Expanded infrastructure and network optimization enable faster fulfillment at national scale.

Consultation processes and policy recalibration signal potential changes to the framework governing North American trade.

Trade actions and infrastructure shifts force rapid recalibration across logistics networks.

Three consecutive months of sales growth signal changing household purchase behavior.

Sustained demand and absorption trends are reshaping investment strategies and capital flows across the sector.

Diverging approaches by Zillow and Redfin expose challenges in transparency, regulation, and public interpretation of risk analytics.

Logistics networks are adapting as dry ice supply limitations disrupt traditional operating models.

Shifting inventory strategies and lease sizes are redefining how users engage with available supply.

Transaction activity is returning unevenly as capital concentrates in assets with clearstructural demand.

Rising distress reflects maturity risk and tighter credit conditions more than widespreaddeterioration in property cash flows.

Labor cooling, cautious policy easing, and stabilizing sentiment point to normalizationrather than downturn.

High vacancies and funding cuts force a rethink of risk and value assumptions.

AI-driven behaviors are redefining how shoppers search, choose, and act.

AI-driven auditing and unified systems mark a shift toward fully integrated operational tools.

Massive capital commitments highlight a strategic drive toward tech-led expansion and market growth.

Shifting monetary signals push investors and developers to rethink borrowing and deal strategies.

A split vote and mixed economic signals highlight the Fed’s evolving strategy.

Rising sustainability goals and intelligent systems are prompting a renewed focus on long-term efficiency and infrastructure adaptation.

Rising expectations for reliability, data access, and seamless execution are redefining how retailers operate and engage customers.

Evolving market pressures and stronger enforcement are redefining buyer timing and seller participation across major marketplaces.

Institutional Capital Rises as Investors Bet on Long-Term Growth

Policy-driven investments aim to strengthen U.S. supply chains for critical minerals.

A potential first-of-its-kind SRT could reveal whether investors are willing to absorb the rising credit concentration behind AI and data-center builds.

Top-line rates look steady, but office, lodging, and even industrial are showing deeper cracks that change the risk profile for 2026.

FHFA-sets-2026-multifamily-caps-88b-each

Surging originations and billion-dollar fundraising signal a structural shift in financing demand.

33M SF underway and stable pricing suggest developers are pacing supply to demand volatility.

Hybrid work cements itself as the dominant force in space demand.

labor drives construction costs 2026.

New forms of tenant activation suggest changing strategies for responding to evolving demand in commercial environments.

New financial commitments may influence the trajectory of established properties in evolving urban contexts.

Construction input prices rise 3.5% YoY, signaling renewed cost pressures and challenging developers to revise budgets, procurement strategies, and lender expectations for 2026.

Institutional capital pivots toward senior housing as sector leads CRE returns, driven by occupancy highs, yield stability, and limited new supply.

Legal sector expansion offsets office market declines; capital, credit, and trophy buildings benefit as law firms double leasing share.

CRE debt markets show revived liquidity as banks and private lenders return, compressing spreads and opening a refinancing window for resilient asset classes.

Prime office assets show early pricing stability as sector bifurcates; record CMBS delinquencies and high vacancy shape capital and underwriting discipline.

A wave of private buyers targets discounted U.S. REITs as credit markets thaw, fueling billion-dollar privatizations and reshaping public-to-private asset pricing.

Reviving deal volume and easing credit conditions spark cautious optimism for cap rate compression across U.S. commercial real estate sectors into 2026.

Home Depot’s 2025 guidance cut spotlights retail CRE risk, as discretionary sales slow and local leasing bifurcates.

Antitrust decision secures Meta’s platform integration, preserving large-block office leasing patterns among U.S. tech leaders.

Decommissioned nuclear plant sale signals evolving capital flows and land-use risk in Mid-Atlantic energy infrastructure.

Auction of 2.1M sf asset signals lender caution for Midtown’s non-trophy office segment, underscoring divergent capital risk and price discovery in Manhattan.

Selective Capital and Redevelopment Drive St. Louis Retail’s Resilience Amid National Headwinds

Resilient US retail sector sees vacancies rise modestly, with new supply at multi-decade lows and disciplined capital underwriting amid evolving consumer and cap rate dynamics.

Institutional capital targets grocery-anchored centers in high-growth Southeast markets; robust sales, high occupancy, and defensive income profile drive portfolio strategy.

Distressed asset sales climb 20% YoY; persistent bid-ask gaps split US CRE market by asset quality and capital behavior.

Institutional disposition in Southeast and Mid-Atlantic signals two-speed capital markets, reshaping multifamily risk and opportunity.

National brokerage M&A activity intensifies in 2024 amid capital market bifurcation; smaller firms struggle for funding as large platforms scale.

Institutional focus buoys Phoenix retail volumes; two-speed market emerges amid lending headwinds

JLL’s Q3 revenue rises 4% YoY; global capital markets and advisory offset weak U.S. leasing, highlighting divergent regional CRE cycles.

Regulatory rent cap splits Los Angeles multifamily market, reshaping asset planning and revenue expectations for institutional owners.

Global capital flows into U.S. real estate persist amid domestic lender pullback.

Institutional asset liquidation highlights ongoing two-speed market in national multifamily sector.

Tech capital gains diverge from broader real estate sector trends.

National aggregate steadies as metro-level lending shows mixed movement.

Institutional debt origination edges up while broader transaction activity varies by asset class.

National hotel pipeline remains mixed as Kansas City sees incremental growth.

Institutional capital pursues large multifamily assets in Sun Belt metros amid mixed liquidity for smaller deals.

National firms drive large-scale leasing, contrasting local warehouse demand.

Local office values reveal a two-speed trend amid rising vacancy rates.

Event signals firm-level risk-control action; local brokerage landscape may see reputational recalibration.

Cross-border capital flows to MENA as US-Canada deal activity remains subdued.

Regulatory uncertainty places upward pressure on multifamily pricing strategies.

Blackstone's latest fund signals sustained capital inflow amid market challenges.

Institutional trophy assets endure capital pressures as local office recovery falters.

office markets persist; institutional lenders complete large refinancing in prime Manhattan submarket..

National distress filings climb, but private capital solutions outpace formal bankruptcy activity.

Institutional capital reassesses New York exposure as rent law debate intensifies.

Institutional capital signals risk repricing in senior housing sector.

Leasing volume remains steady while availability signals bifurcation in the market.

Mixed trends in the U.S. office market show a bifurcation in value and leasing dynamics.

Divergent trends in institutional and small deal volumes signal mixed market recovery.

Analysis of CRE's bifurcated landscape reveals contrasting sector performances.

Institutional lender backs urban infill amid tightening construction lending.

Two-Speed Market as Nonbank Capital Expands Role in CRE Lending

Increased leasing activity boosts JLL's revenue and outlook for 2025.

Diverging trends in global CRE investment volumes signal market differentiation.

Institutional capital steps in to fill CRE lending gap as banks retreat

Divergent trends reveal mixed recovery in retail leasing and occupancy.

Record closures signal bifurcation in office market dynamics affecting capital behavior.

Mixed signals in commercial real estate as industrial and data centers gain traction amid declining overall deal volume.

Tech firm Sigma Computing's lease growth reflects Manhattan's office market recovery.

Major financing signals ongoing confidence in Miami’s residential market.

Softening residential sales drive significant earnings decline for brokerage.

MCB’s increased bid reflects growing confidence in retail assets.Dateline

Analysis of leasing trends reflects shifting capital flows in U.S. office markets.

Emerging signs of office demand recovery are moderating the risk premium in major U.S. gateway markets.

Surging vacancy rates challenge office asset values, reshaping capital flows and leasing strategies in gateway and secondary markets.

Disciplined pricing persists as warehouse absorption slows; developers calibrate risk while institutional capital monitors excess inventory.

Midwest assets attract disciplined capital as industrial fundamentals outperform softer national metrics amid persistent rate headwinds.

Subdued leasing gains face rising financing barriers as capital constraints persist in gateway office markets.

Distress-driven sales and rising vacancies force a repricing in core U.S. office markets, signaling shifts in capital and leasing behavior.

E-commerce expansion steadies Midwest warehouse demand as construction revives.

Lower yields steady cap rates and reopen deal flow, but underwriting stays defensive.

Slower relief, selective credit—capital finds footing amid Fed debate

Tight vacancies and disciplined supply keep Texas retail steady as shoppers slow.

Flight-to-quality solidifies as trophy assets stabilize occupancy while older offices confront obsolescence and capital strain.

National rents fall 0.8% in October as new supply surges; multifamily operators shift from growth to preservation

Leisure demand keeps Florida’s hospitality market near full occupancy as costs and capital tighten

Corporate investment and population growth converge, positioning Texas metros as national CRE accelerators.

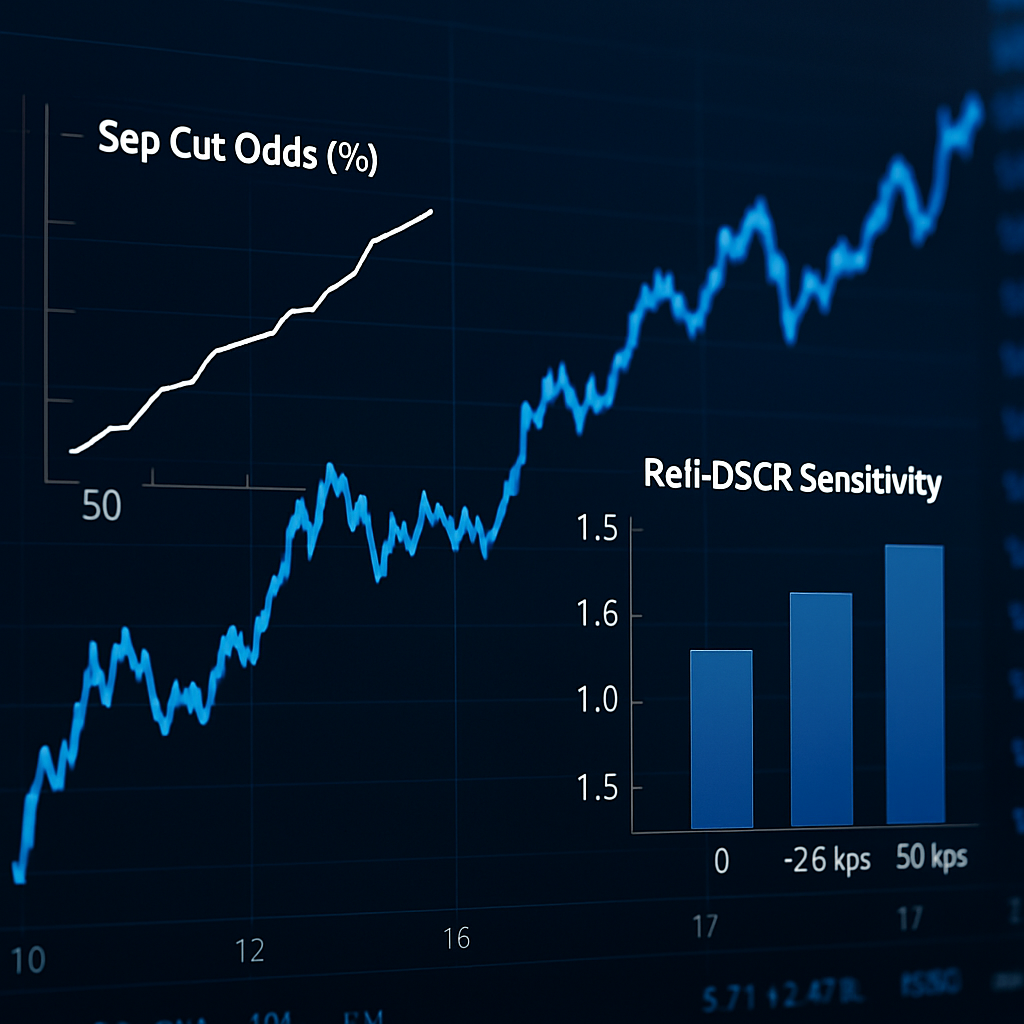

Supply surge flips pricing power to renters; debt and DSCR now the fulcrum

Institutional owners are crystallizing 30–60% losses on Manhattan towers, resetting office values and reopening deal flow.

Robust presales and private wealth equity de-risk a $500M Miami Beach ultra-luxury project before construction begins.

A $70 million buyout secures full ownership of 3025 JFK Blvd—testing conviction in a soft lab market with 34 percent vacancy.

Rising office loan distress is reshaping lender risk tolerance and underwriting discipline.

Tight occupancy and modest rent gains reaffirm retail’s post-pandemic resilience.

Allocation gaps, easing rates, and a thawing credit market are setting the stage for renewed institutional capital flow into U.S. CRE.

Sruge in new supply drives first national rent decline in 15 years

A 40% rent jump in North DFW’s luxury suburbs reveals a new equation linking construction inflation to tenant demand.

As banks shrink loan books by high-single digits, private credit floods into commercial real estate—resetting risk, cost, and control.

Positive net absorption and vanishing new supply mark a structural inflection in U.S. office fundamentals.

Development pipeline contracts further while vacancy remains elevated—select markets lead the adjustment.

Office vacancy declines, leasing activity rebounds—suggesting a new phase of market stabilisation.

Trophy trades return, reprice risk, and reset comps as institutional capital re-engages in Midtown

NYC is rewriting the office cycle: deep flight-to-quality meets real, dated rent prints.

Bargain-basement sales expose a capital reset but hint at slow healing

Supply finally outruns demand as concessions widen; underwriting shifts to defense.

Low vacancy and disciplined development keep rents near records despite slower deal flow.

Distress migrates from offices to billion-dollar builds as financing tightens and maturities bite.

Capital remains confident in necessity retail as consumer restraint tempers holiday expectations

Slug: Traditional lenders retreat as private debt funds reshape CRE’s capital hierarchy Dateline: October 22 2025 — CRE360 Editorial Signal

Multi-bank exposure to a $270 million loan scheme exposes structural fragility in regional lenders’ CRE portfolios.

Strong population inflows sustain capital and construction momentum, but hospitality and underwriting caution temper the region’s exuberance.

Repricing has brought discipline to a sector now trading on yield rather than fear.

A record 11.13 % CMBS delinquency rate signals a historic office shake-out and a prolonged refinancing crunch.

September’s 8.12% office delinquency rate marks a decisive turn in CRE credit stress.

Store closures accelerate — yet the remaining footprint proves stronger

Slower borrowing costs thaw CRE capital markets

BlackRock, Nvidia, and Microsoft’s record acquisition cements data centers as a core institutional asset class — merging tech and real estate capital.

Leasing surge confirms recovery and renews confidence in NYC’s core asset class

Loan modifications jump 66% as lenders manage distress, not defaults

As rents post their steepest fall in 15 years, capital tightens underwriting standards and resets yield expectations.

Powell’s signal that quantitative tightening may end reshapes debt costs and sentiment across real estate finance

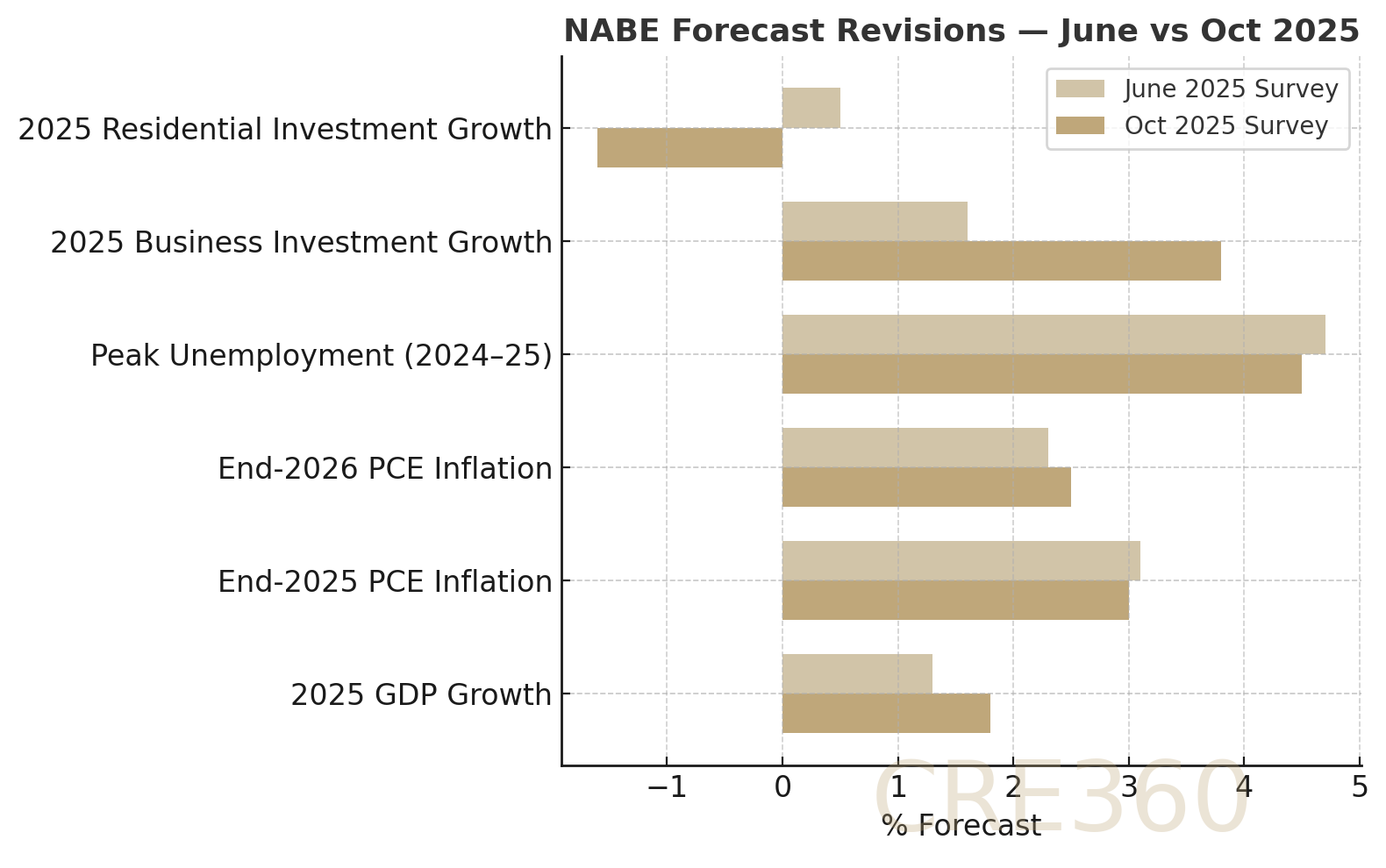

Upgraded GDP forecasts lift CRE confidence, but sticky 3% inflation keeps borrowing costs high.

Massive debt-for-equity swap offers lifeline as bondholders absorb 78% losses, reshaping global views on China’s credit risk.

Banker departures and M&A contraction signal leaner underwriting conditions across capital markets and CRE.

Lenders maintain strong appetite for large, stabilized warehouse portfolios amid a moderating but resilient industrial market.

Multifamily rents stall as 475k new units hit the market, driving concessions and soft occupancy.

Lower policy rates ease borrowing costs, but CRE loan distress and tight credit temper optimism.

Green Street’s CPPI edges up, confirming pricing equilibrium and renewed deal flow in U.S. commercial real estate.

New disclosure rule lets modified CRE loans disappear from public view after 12 months, masking true debt stress.

San Francisco’s 800 Market St. sale at $344/sf signals a new pricing floor as office distress deepens.

$27.7 B in CRE loans reworked amid 7% refinancing rates and maturing 2025 debt.

Lenders are extending maturities to avoid defaults, doubling CRE loan modifications and deferring risk into 2026–2028.

Brookfield cuts U.S. office leadership and outsourcing ops, shifting from direct ownership to capital-light asset management.

Suspension of key federal grants halts Chicago’s subway expansion and raises new political risk for infrastructure capital.

Federal paralysis halts permits, data, and loan programs—raising execution risk and widening spreads across U.S. commercial real estate.

Divergent sectors force Fed to prioritize inflation control over property market relief.

Exploding construction costs force Miami developers to reprice projects, rethink feasibility, and cap leverage.

Exploding construction costs force Miami developers to reprice projects, rethink feasibility, and cap leverage.

Record-pace leasing and falling vacancies mark a decisive Class A recovery in Manhattan office demand.

Exploding construction costs force Miami developers to reprice projects, rethink feasibility, and cap leverage.

SF and LA face historic office vacancies; conversions, deep discounts, and high-risk underwriting dominate current capital playbooks.

Venezuelan outflows trigger vacancies in Doral, accelerating Florida’s broader multifamily rent plateau.

Class A assets attract bids near peak while transitional deals sit idle.

CRE transaction volumes up 10% in 2025 as rates plateau, drawing capital back to multifamily, industrial, and debt-backed dealmaking.

7M+ SF of shuttered stores strain REITs, CMBS, and retenanting models in secondary markets.

2024’s record deliveries pushed vacancies to ~12%, but with new supply plunging 50%, Texas multifamily is stabilizing fast.

Institutional landlords now control 17% of U.S. logistics assets, reshaping valuation, yield, and competition.

FTC suit, CoStar clash, and rival momentum threaten Zillow’s dominance—and could reshape how listings platforms monetize housing data.

Federal layoffs and withheld paychecks push listings up ~55% as buyer sentiment falters across the capital region.

High-end housing faces thinning buyers, forcing repricing and longer absorption timelines.

Shrinking foreign inflows leave U.S. CRE reliant on selective capital and domestic syndicates.

Investors pivot from secondary retail toward AI, ESG-compliant assets as capital reallocates globally.

Investors pivot from secondary retail toward AI, ESG-compliant assets as capital reallocates globally.

Landmark deal curbs algorithmic rent setting, reshaping underwriting and tenant retention in multifamily.

Trophy Manhattan offices repriced; equity-led recaps set new comps and reopen execution for patient operators.

IKEA’s $213M SoHo buy blends flagship retail with new boutique offices, testing Manhattan’s post-pandemic urban demand.

Microsoft’s exit leaves Bravern Commons empty, triggering default and underscoring risks of tenant concentration in office underwriting.

Record IPO capitalizes on AI demand, but execution risks loom over phased Amarillo megacampus build.

Antitrust suit targets $100M deal alleged to inflate rental listing costs for multifamily owners.

Hotel RevPAR dipped –1.4% YoY as occupancy softness offsets resilient ADR, pressuring underwriting assumptions.

U.S. hospitality now employs 2.1M more workers than 2020, but at 35% higher wages.

Large, institutional assets are rebounding, while smaller property values remain under pressure.

Sustainability shifts from compliance cost to income driver, shaping underwriting, financing, and exit values.

Square 67 trades swiftly, proving Sunbelt retail’s resilience and liquidity amid high rates.

Conversions surge as office vacancies mount and housing incentives drive Manhattan’s largest adaptive reuse wave since 2008.

Net-leased childcare centers attract repeat buyers with yield premiums and long leases, even as borrowing costs remain high.

August saw steady $100M+ deals and active mid-market trades, signaling disciplined but ongoing liquidity in U.S. CRE.

Debt funds and CMBS re-open the channel, easing execution for qualify-to-close CRE.

Trophy listing will benchmark SF office values and financing.

Office vacancy reached 20.7% in Q2 2025, straining cash flows, refinancing, and valuations amid a $290B debt wall.

Vacancy rises modestly, but strong demand and record permits keep Northwest Arkansas resilient against U.S. market slump.

Dallas landlord redeploys into industrial, betting on tight shallow-bay supply and sustained rent growth.

Store closures and job cuts free capital for drive-thru and tech reinvestment.

Gemini venture pools distressed Class A towers, offering liquidity lifeline to landlords under pressure.

Rent burdens and supply shortfall strain multifamily investors despite Fed rate cuts.

Bankruptcy sale of Pinnacle’s rent-stabilized portfolio resets NYC underwriting and lender recoveries.

Landmark construction financing highlights lender confidence in luxury mountain resorts despite high-rate backdrop.

Major NYC hotel trade signals renewed investor confidence as borrowing costs ease and urban demand outperforms U.S. averages.

Columbia Sussex acquires 744-room resort, betting on a major Hilton-flag reposition despite softening local demand.

Occupancy slides to 76% as Strip resorts waive fees and cut rates to spur demand.

Landmark construction financing highlights lender confidence in luxury mountain resorts despite high-rate backdrop.

Surplus lab supply drives double-digit vacancy, forcing owners to weigh conversions, concessions, and distressed sales.

$18B U.S. PACE experience drives new global initiative to unify property-linked retrofit financing.

Scale bid unites 340K agents, $10B enterprise—capital tests if consolidation can offset housing slump.

Insurance premiums up 88% in 5 years, $1.4T in real estate at risk. Climate resilience moves from ESG talk to underwriting math.

Public bond capital backfills vacant office, accelerating a 2027 tech campus at below new-build cost for taxpayers.

Expansion cements SE Wisconsin as a hyperscale hub, with spillover demand for industrial land, power, and supplier space.

First major public-to-private office deal signals patient capital returning to NYC and SF trophy towers.

Big-check capital targets manufactured housing for durable yields and low capex.

Fortress buys four UPS assets; pricing and credit signal resilient industrial financing.

Expansion cements SE Wisconsin as a hyperscale hub, with spillover demand for industrial land, power, and supplier space.

Origination and issuance tick up as non-banks re-enter; banks stay selective, terms improve modestly for well-structured deals.

Cooling permits and a thinning MF pipeline ease 2026 supply pressure—supportive for rent stabilization in overbuilt nodes.

Easing base rates lower agency coupons and bridge carry, nudging DSCR over the line in stabilized markets.

Easing cycle begins; refinancing window cracks open but spreads and underwriting remain tight for CRE.

Corporate balance sheets, not debt markets, are fueling the Midwest’s emergence as a hyperscale AI infrastructure hub.

PJM capacity costs jump 6× as hyperscale projects flood Pennsylvania, raising financing risk for CRE linked to power-intensive users.

Public-private deal unlocks stadium plus 6,000 homes; muni bonds fund infrastructure, private equity funds venue.

Toll exits rentals, Kennedy Wilson gains $5B pipeline — a late-cycle bet on multifamily resilience.

Maple Plaza trades at ~$700/sf, defying office downturn with flight-to-quality pricing.

Rising vacancies press leasing and pricing strategies in U.S. industrial markets.

Office demand lags as key sectors underperform, impacting financing and leasing dynamics.

Brookfield’s $400 million revamp fills 660 Fifth, highlighting NYC's flight-to-quality in office leasing.

Persistent high rates stall transaction volume, hindering CRE financing.

New co-investment approach by Florida SBA impacts CRE financing with fee reductions and competitive loan terms.

Prime assets outperform in leasing as bifurcation widens in U.S. CRE markets.

Green Street’s CPPI shows flat pricing — CRE360 interprets it as values bouncing along the bottom.

Trepp reports office and multifamily delinquencies hit record highs — CRE360 calls it a bifurcated debt market.

Colliers flags rent declines leveling off, but CRE360 notes recovery will be slow and bifurcated.

Cushman & Wakefield forecasts no recession but choppy waters — CRE360 stresses strategy and contingency as the cycle turns.

Bidding activity ticks up for the first time in 2025 — CRE360 calls it a tentative bottom, not a rebound.

Net-lease investment increases by 27% — CRE360 warns the boom is uneven across property types.

Investment & lending activity continue to improve — CRE360 notes recovery is uneven and sector-specific.

NYC offices see significant value drops, impacting CRE strategies and financing.

Collapse from $1.2B to $195M underlines urban retail distress and mall financing risks.

High vacancies and loan defaults drive severe CMBS market disruption in Seattle.

Demand and supply equilibrium fosters stability in self-storage financing and execution

High-leverage financing underscores market confidence in Phoenix's industrial assets.

Increased supply curbs rent growth, impacting multifamily returns in high-growth markets.

CBRE flags vacancy stabilization, but capital pressures keep Zurich office yields too tight for new inflows.

Fed's anticipated rate cut to lower borrowing costs, impacting CRE financing positively.

Three rate cuts in 2025 expected; impacts CRE cost of capital and financing plans.Date & Sources: September 12, 2025. Reuters, Morgan Stanley, Deutsche Bank.

Hotels Flat; Luxury Outperforms. Post-summer softness persists; top tiers hold rate as economy segments slip.

Tech leasing is refilling top-tier offices, improving rent rolls and refinance stories for prime assets.

Fulton Market trade shows cap-rate stability as rent growth reopens bid-ask spreads.

Fresh equity targets Sunbelt apartments as debt maturities bite.

Regional banks remain cautious on CRE, pushing more flow to private credit.

30-year mortgage rates dropped to 6.49%, the lowest since October 2024. Refinancing surged and purchase applications gained, signaling a rate-sensitive rebound in demand.

Consumer prices overshot expectations, but labor weakness keeps the Fed on track for a likely September rate cut.

Cottonwood Group raised $1.0B for distressed CRE bets as $2T of loan maturities approach. Already $300M deployed with 20% IRR returns, targeting high-growth U.S. markets.

Private credit finances a ~280k SF condo across Franklin–Fulton–Broadway after a 2025 basis reset, signaling lender appetite for core-Manhattan scale.

Owners consolidate and upsize debt on twin luxury towers, locking long-term financing well before maturities hit..

Cottonwood raises $1B “special situations” fund, doubling target as investors chase distress opportunities in a frozen CRE market.

Retail REITs post record 96.6% occupancy as new supply hits historic lows; landlords gain leverage with steady NOI growth and limited competition.

Luxury hotels are driving hospitality’s rebound, posting RevPAR and ADR gains while midscale and economy segments slip under cost pressures and weak demand. The market is splitting into clear winners and losers.

Industrial financing resilience: Starwood’s $930M refinancing shows lenders’ deep appetite for logistics portfolios, even at higher rates, with below-market rents providing embedded growth.

Silver Star’s default highlights U.S. office distress: 21% national vacancy, Sunbelt weakness, and lenders tightening on extensions.

U.S. apartment rents fell again in August, as 950k new units under delivery push vacancies higher and blunt landlords’ pricing power.

High-end brands continue to secure scarce trophy retail locations, sustaining rent growth even as international tourism lags.

Brent’s bounce to ~$66 offsets a sharp summer slide, easing hotel utility pressure. Forward curves point lower, giving operators a narrow cost tailwind into Q4.

Markets now assign ~90% odds to a September Fed cut, with some banks calling 50 bps. Relief boosts refi math but doesn’t change long-run cap-rate expectations.

Spot gold holds just below all-time highs, reflecting rate cut expectations and macro caution. Allocators are tilting into real assets and secured credit, creating knock-on signals for CRE capital flows.

Medical office assets in Chicago post record absorption, steady rents, and renewed investor demand as general offices falter.

CMBS delinquencies rose for the sixth straight month to 7.29% in August. Office hit a record 11.66% and multifamily climbed to a nine-year high at 6.86%, tightening credit and accelerating workouts.

Incremental gains show market resilience; debt costly but available keeps transactions flowing.

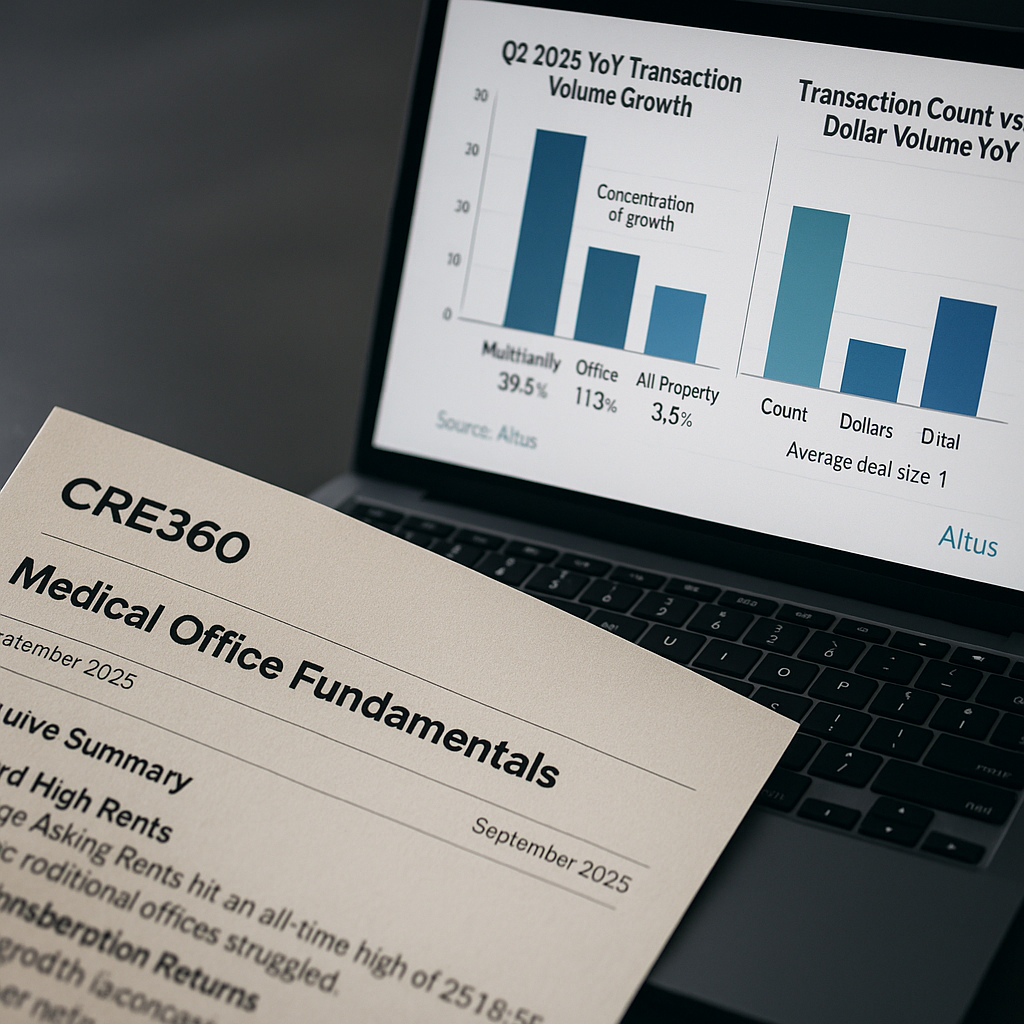

Dollar volume rose even as the market did fewer trades. Large, institutional deals carried Q2 while small and mid-market liquidity thinned. Sep 2025. Source: Altus Group Investment Trends Report (Q2 2025).

Visitor volume fell double digits into July. Strip hotel metrics and national RevPAR point to a softer near-term runway while operators tout value and big-event tailwinds. Sept 2025. Sources below.

Average MOB rents reached record highs, demand turned positive, and capital inflows accelerated in Q2 2025, confirming medical office as a defensive outperformer.

Downtown LA’s Ernst & Young Plaza debt sale underscores a collapse in trophy office valuations, with bids expected at up to 60% below pre-pandemic pricing.

Occupancy ~63% and RevPAR up just 0.2% YoY amid High Season Travel Records

The RCA CPPI turned positive again. Two straight YoY gains signal a floor, led by retail and industrial while office bifurcation persists

The under-construction pipeline has fallen ~60% from the 2023 peak to ~543k units, setting up a 2026–27 supply drought after 2025’s final wave of deliveries. Date: 09/2025. Source: RealPage Market Analytics (Q2 2025).

JLL reports lifestyle office markets command 32% rent premiums, twice-as-fast lease-ups, and lower vacancy—signaling a structural shift in office demand.

Q2 sales fell to $9.6B, the second-weakest quarter in 10+ years, as financing costs thinned the buyer pool. Cap rates averaged 6.93% and rose only 3 bps, indicating stabilization.

U.S. rents fell in August as deliveries peaked. Supply-heavy Sun Belt metros are contracting while supply-constrained coasts and the Midwest hold up. 09/2025. Sources: CoStar

Austin-based firm overshoots targets, signaling LP confidence in mid-market operators despite higher

The nation’s largest apartment manager is rolling out pricing calculators, AI tools, and resident-facing transparency measures to sustain NOI in a cooling rental market.

Nomura revives CMBS platform with Barclays veterans, targeting trophy assets as U.S. banks retrench.

The nation’s largest apartment manager is rolling out pricing calculators, AI tools, and resident-facing transparency measures to sustain NOI in a cooling rental market.

Tri-State industrial market shows resilience with 8.7% vacancy, stable rents, and robust 3PL demand amid rising port throughput and strategic lending landscape.

Selective lending continues for top-tier multifamily and industrial assets as bank hapoalim and starwood provide $720M in strategic NYC refinancing amid challenging CRE market.

U.S. multifamily market cools as rent growth stagnates at 0.7% YoY, with record supply and softening demand causing occupancy and concession shifts in 2024.

Norwegian Wealth Fund acquires Midtown Tower at 34% discount, signaling major NYC office market shift and key investment trend in commercial real estate.

Labor Day 2025 shatters U.S. travel records with 10.4M TSA screenings, signaling a robust tourism rebound and return to pre-pandemic travel enthusiasm.

Florida Gulf Coast $1B resort sale tests market resilience as CMBS delinquencies hit 7.29%, with office and multifamily sectors driving unprecedented commercial real estate defaults.

CMBS market faces mounting distress as U.S. delinquency rates hit 7.29%, with office and multifamily sectors driving record defaults amid challenging refinancing landscape.

Retail CRE shows surprising resilience in 2025, with CMBS delinquencies dropping to 6.42% amid strong consumer spending and strategic asset repositioning.

Private equity primed to deploy $250B+ in commercial real estate, targeting repriced assets and recapitalizations amid 2025-26 market recovery.

U.S. commercial real estate investment sales surge 16% in H1 2025, with $163.6B in transactions as private buyers drive market recovery amid selective price stabilization.

SB 15, SB 840, and HB 24 reshape zoning, conversions, and neighbor protests; most provisions take effect September 1, 2025.

Distress is high but stabilizing, with banks extending viable loans and bond metrics bifurcating; the $957B 2025 maturity wall keeps pressure on underwriting and equity.

U.S. retail remains resilient with 6.1% vacancy, strip centers thriving, and institutional capital returning amid strong consumer spending and steady NOI growth.

U.S. office vacancy hits record 20.6% in Q2 2025, with NYC showing early stabilization and adaptive reuse transforming obsolete spaces amid market shift.

Southern California industrial market shows resilience: MetLife's $165.5M portfolio sale signals strong investor confidence amid rising vacancies and record-high warehouse rents.

Discover Charlotte's multifamily market resurgence: Investors return as supply peaks, rents stabilize, and opportunities emerge in this promising Sunbelt real estate landscape.

Commercial real estate lending rebounds in Q2 2024, with 66% year-over-year growth as banks and debt funds return to market, driven by stabilizing rates and improved underwriting confidence.

CMBS market reaches $58.8B in H1 2025 with record single-asset deals, despite rising office loan defaults and 7.3% overall delinquency rate.

Source: CBRE U.S. Medical Outpatient Buildings Q2 2025 Report

Sources: Altus Group, GlobeNewswire, GlobeSt

Source: RealPage, CRE Daily Recap

Source: Northmarq Q2 2025 MarketSnapshot; GlobeSt recap

Source: Yardi Matrix

Date: Aug 9, 2025 | Sources: CRE Daily; Seniors Housing Business

Trusted Daily

40,000+

Daily Subscribers

Brokers, investors, developers, and lenders open CRE 360 Signal™ every morning for the market intelligence that moves their decisions.

Free. Independent. Editorially rigorous.

Follow the Signal

Add your profile URLs from the Editorial Desk → Social links.